How to Start Investing with Little Money

The persistent myth that you need to be “rich to get rich” has kept millions of potential investors on the sidelines for decades. In the past, the barriers to entry were indeed high—steep commissions, minimum account balances, and the high cost of individual shares of blue-chip companies made the stock market feel like a private club for the elite.

However, we are living in the golden age of the retail investor. Thanks to technological disruption and a shift in brokerage models, the doors have swung wide open. Today, you can start your journey toward financial independence with as little as $5.

If you have been waiting for a “windfall” to start your portfolio, you are losing your most precious asset: time. This guide will show you exactly how to start investing with little money, leveraging the power of modern financial tools to build a legacy from scratch.

The Power of Compounding: Why Your “Small” Start is a Big Deal

Many people scoff at the idea of investing $20 or $50 a month, thinking it won’t make a difference. This is a fundamental misunderstanding of how wealth is built. The secret isn’t the size of your initial deposit; it is the compounding of returns over time.

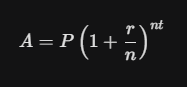

Compounding happens when the earnings on your investments start earning their own money. To see the impact, we can look at the compound interest formula:

Where:

-

A = The future value of the investment

-

P = Your initial principal (small as it may be)

-

r = Annual interest rate (decimal)

-

n = Number of times interest is compounded per year

-

t = Number of years the money is invested

The “Early Bird” Advantage

Consider two friends:

-

Friend A starts at age 22, investing just $100 a month. By age 62, assuming a 7% average annual return, they have roughly $240,000.

-

Friend B waits until age 32 to start but invests $200 a month (double the amount). By age 62, they have only $225,000.

Despite putting in more total capital, Friend B can never “catch up” to the decade of compounding Friend A enjoyed. This is why starting today with $10 is better than starting in five years with $100.

Advanced SEO Strategy: Step-by-Step Checklist Before You Invest

Before you put your hard-earned money into the market, you need a “financial moat” to protect your progress. Investing without a foundation is like building a house on sand.

1. Build a “Starter” Emergency Fund

The stock market is volatile. If you invest your grocery money and the market dips 10% next week, you might be forced to sell at a loss just to eat. Aim for at least $1,000 or one month of expenses in a high-yield savings account before you buy your first stock.

2. Slay High-Interest Debt

If you are paying 22% interest on a credit card and the stock market averages 10% returns, you are effectively “losing” 12% a year. Pay off any debt with an interest rate higher than 7% (like credit cards or payday loans) before you focus heavily on investing.

3. Utilize Employer Matching (The Only “Free Lunch”)

If your employer offers a 401(k) match, that is a 100% return on your investment before the market even moves. Even if you have very little money, contribute enough to get the full match. It is the most efficient way to grow a small account.

Fractional Shares: Owning the World’s Biggest Companies for Pennies

In the past, if a single share of a major tech company cost $3,000 and you only had $50, you simply couldn’t buy it. You were forced to buy lower-quality “penny stocks” which are often scams or highly volatile gambles.

Fractional shares changed everything. Now, major brokerages allow you to buy “slices” of a stock. If you have $10, you can own $10 worth of Amazon, Google, or Berkshire Hathaway.

Why Fractional Shares are a Beginner’s Best Friend:

-

Diversification: You can spread $100 across 20 different world-class companies.

-

Psychology: You get to own the brands you actually use and understand.

-

Low Barrier: You can start immediately without waiting to save up hundreds for a single share.

The Best Micro-Investing Platforms for 2026

To start small, you need a platform that won’t eat your profits with fees. Look for brokerages with zero commissions and no account minimums.

| Platform Type | Best For… | Features |

| Traditional Giants (Fidelity, Schwab) | Long-term growth | Full research tools, fractional shares, robust security. |

| Micro-Investing Apps (Acorns, Stash) | Passive “spare change” | Automatically rounds up your purchases and invests the change. |

| Robo-Advisors (Betterment, Wealthfront) | Hands-off investors | Automatically manages a diversified portfolio based on your risk. |

For most beginners, Fidelity or Charles Schwab are excellent choices because they offer “slices” of stocks and have no hidden fees that could drain a small account.

Index Funds and ETFs: The “Set It and Forget It” Strategy

If you don’t want to spend hours researching individual companies, Exchange-Traded Funds (ETFs) are your secret weapon. An ETF is a basket of stocks that you can buy with one single transaction.

The S&P 500 Index Fund

The most popular index is the S&P 500, which tracks the 500 largest companies in the United States. When you buy one share of an S&P 500 ETF (like VOO or SPY), you are instantly diversified across tech, healthcare, energy, and retail.

For a small investor, this is far safer than picking one or two stocks. If one company in the 500 fails, the other 499 carry the load. Historically, the S&P 500 has returned an average of about 10% per year over long periods.

How to Find “Extra” Money to Invest Every Week

If you think you have “zero” money to invest, it’s time for a budget audit. Small, recurring leaks in your finances are the biggest obstacles to wealth.

-

The “Subscription Audit”: Use an app to track your recurring payments. Canceling one $15 streaming service you don’t use and investing that $15 a month could grow to over $35,000 over 40 years.

-

The “Round-Up” Method: If you spend $4.50 on a coffee, treat it as $5.00 and put the extra $0.50 into your brokerage account.

-

Generic vs. Brand Name: Switching to store-brand groceries can save the average person $20–$50 a week. Redirecting that “found money” into an index fund is how fortunes are made.

Common Mistakes to Avoid When Investing Small Amounts

When you start with a small amount of capital, you might feel a “rush” to grow it quickly. This often leads to the most common beginner traps:

1. Chasing “Meme” Stocks and Crypto

High-volatility assets can go up 100% in a day, but they can also drop to zero. For a small investor, losing your entire $500 stake can be demoralizing and lead to quitting entirely. Stick to the “boring” path of index funds for 90% of your portfolio.

2. Excessive Trading

Even with $0 commissions, constant buying and selling (day trading) usually results in losses for beginners. Every time you sell, you may trigger a tax event. The most successful small investors are those who buy and never look at the app.

3. Ignoring Expense Ratios

Even “free” ETFs have internal management fees called expense ratios. If an ETF has a 1% fee, it might not seem like much, but over decades, it can eat up a third of your total returns. Look for funds with expense ratios below 0.10%.

The “Dollar-Cost Averaging” (DCA) Advantage

One of the best ways to invest with little money is Dollar-Cost Averaging. This means you invest the same amount of money at regular intervals (e.g., $25 every Friday), regardless of what the market is doing.

-

When the market is up, your $25 buys fewer shares.

-

When the market is down, your $25 buys more shares.

This strategy removes the emotional stress of trying to “time the market” and ensures that you are buying the bulk of your shares when they are at a discount.

Psychology of the Small Investor: Overcoming the “Comparison Trap”

In the age of social media, it is easy to feel “behind” when you see influencers posting about their $100,000 portfolios. Remember that investing is a solo race.

Your $500 portfolio is infinitely better than the $0 portfolio of the person who is waiting for the “perfect time” to start. The goal of investing with little money is to build the habit. Once you have the habit of investing $20 a week, increasing that to $200 a week as your career progresses becomes second nature.

Start Small, Think Big, and Stay Patient

Building wealth with little money isn’t just a possibility; it is the way most of the world’s millionaires started. By utilizing fractional shares, low-cost index funds, and the power of compounding, you are bypassing the gatekeepers of the past and taking control of your financial destiny.

The best time to start was ten years ago. The second best time is right now. Open a brokerage account, set up a recurring $5 or $10 transfer, and let the incredible machinery of the global economy begin working for you.

Quick Start Checklist:

-

Open a No-Fee Brokerage Account (e.g., Fidelity or Schwab).

-

Automate a Weekly Transfer (even if it’s just $5).

-

Buy a Diversified ETF (like a Total Stock Market or S&P 500 fund).

-

Reinvest Your Dividends (use the “DRIP” feature).

-

Be Patient. Time is your greatest ally.