Choosing Your First Brokerage: The Ultimate Guide to Investing and Building Wealth

image for illustrative purposes only.

Starting your journey into the world of investing is one of the most powerful financial decisions you can make. The math of building long-term wealth is straightforward: the earlier you begin, the more time your capital has to benefit from the effects of compounding returns. However, for a beginner, the initial hurdle isn’t understanding market mechanics or calculating dividend yields. The real challenge lies in choosing the right infrastructure—specifically, selecting a brokerage platform that aligns with your educational needs, budget, and financial goals.

The modern financial ecosystem offers an unprecedented level of access to capital markets. Decades ago, placing a stock trade required calling a human broker on the phone and paying a hefty transaction fee. Today, digital platforms have democratized trading, reducing commission costs to zero and bringing Wall Street straight to your smartphone.

Yet, this abundance of choice creates a classic paradox. With dozens of applications competing for your attention, how do you separate platforms designed to protect and grow your capital from those that encourage risky, short-term speculation? This comprehensive guide breaks down the structural features of top-tier platforms, evaluates the economic impact of hidden fees, and details the specific attributes that make a brokerage ideal for someone just starting out.

What Makes a Brokerage Account Perfect for Beginner Investors?

Before looking at specific platforms, it is vital to define the criteria that make a trading platform suitable for someone managing their first portfolio. A common mistake among new investors is selecting a platform based solely on brand popularity or a slick user interface. True platform quality, however, is determined by structural alignment with long-term wealth accumulation.

1. Low Cost Barriers and Zero Commissions

For an account with a modest starting balance, fees are the single greatest enemy of growth. If you invest $100 and a platform charges a $5 transaction fee, you instantly lose 5% of your principal before the asset even has a chance to move. A beginner-friendly brokerage must offer commission-free trading on core assets like equities and Exchange-Traded Funds (ETFs). Furthermore, the platform should have no account maintenance fees, no inactivity fees, and zero minimum deposit requirements.

2. Comprehensive Educational Infrastructure

The transition from saving money to investing money requires a shift in mindset. Exceptional brokerages do not treat education as a secondary feature; they integrate it into the core user experience. Beginners need clear, objective explanations of market terms, risk management, and asset diversification. This content should be free of marketing jargon and structured to help users make informed decisions rather than impulsive trades.

3. Robust Security and Regulatory Compliance

Your financial capital must be safe from institutional insolvency or cyber threats. Any platform you utilize must carry top-tier regulatory credentials. This includes registration with the Securities and Exchange Commission (SEC) and active membership in the Financial Industry Regulatory Authority (FINRA).

Crucially, the brokerage must be a member of the Securities Investor Protection Corporation (SIPC). The SIPC protects customers of its members up to $500,000 (including $250,000 for claims for cash) if the brokerage firm fails financially. Note that SIPC insurance protects against the failure of the broker-dealer, not against a decline in the market value of your investments.

How to Evaluate Investment Fees That Quietly Drain Your Portfolio

When a platform advertises “zero-commission trading,” it means they do not charge a flat fee to execute a standard buy or sell order for a domestic stock. It does not mean the platform operates entirely as a charity. To protect your capital, you must understand the alternative ways brokerages monetize their users and how these mechanisms affect your returns.

Payment for Order Flow (PFOF)

Many commission-free brokerages generate a substantial portion of their revenue via Payment for Order Flow. When you submit a market order, the broker routes that order to a high-frequency market maker rather than directly to a public exchange. The market maker executes the trade and passes a fraction of a cent per share back to your broker. While this process keeps front-end commissions at zero, it can occasionally result in slightly worse execution prices on massive orders. For a casual buy-and-hold beginner investing regular sums, the impact of PFOF is generally negligible, but it is a structural mechanism to be aware of.

Margin Interest Rates

Margin trading involves borrowing money from your brokerage to purchase securities, using your existing portfolio as collateral. This is a highly advanced, high-risk strategy that beginners should avoid entirely. However, platforms vary wildly in the interest rates they charge for borrowed money. If you accidentally execute trades on margin or sign up for a premium account tier that enables margin by default, high interest rates can quickly compound against you.

Expense Ratios in Mutual Funds and ETFs

While this is a function of the underlying asset rather than the broker itself, many platforms offer proprietary funds. An expense ratio is the annual fee charged by an investment fund to cover its management expenses, expressed as a percentage of your total investment in that fund. For instance, a fund with an expense ratio of 0.50% will charge you $5 annually for every $1,000 invested.

When building a beginner portfolio, your goal should be to favor low-cost index funds or ETFs with expense ratios below 0.10%. Over a 30-year investment horizon, the difference between a 0.05% fee and a 0.75% fee can translate into tens of thousands of dollars in lost gains due to the interruption of compounding growth.

Best Low-Fee Investment Platforms to Safely Start Building Wealth

To help you navigate the landscape, let us analyze the specific market leaders that consistently rank as excellent entry points for new investors. Each of these institutions approaches user onboarding from a distinct angle, offering unique advantages depending on your preferred style of management.

| Brokerage Platform | Account Minimum | Trading Commissions | Best Structural Feature |

|---|---|---|---|

| Fidelity Investments | $0 | $0 for Equities/ETFs | Fractional shares & Zero-fee index funds |

| Charles Schwab | $0 | $0 for Equities/ETFs | Exceptional customer service & Schwab Starter Kit |

| Vanguard | $0 | $0 for Mutual Funds/ETFs | Built for long-term buy-and-hold index investing |

| Robinhood | $0 | $0 for Equities/ETFs | Streamlined, mobile-first interface & IRA matching |

Fidelity Investments: The Best Overall Traditional Powerhouse

Fidelity stands out as an exceptionally well-rounded option for beginners who want premium tools without paying premium fees. Unlike many traditional institutions that require substantial initial deposits, Fidelity has completely removed account minimums and core trading fees.

- Fidelity Zero Funds: Fidelity was a pioneer in launching index mutual funds with an absolute 0% expense ratio. These funds track broad market segments, allowing beginners to gain diversified exposure to the stock market with zero ongoing management costs.

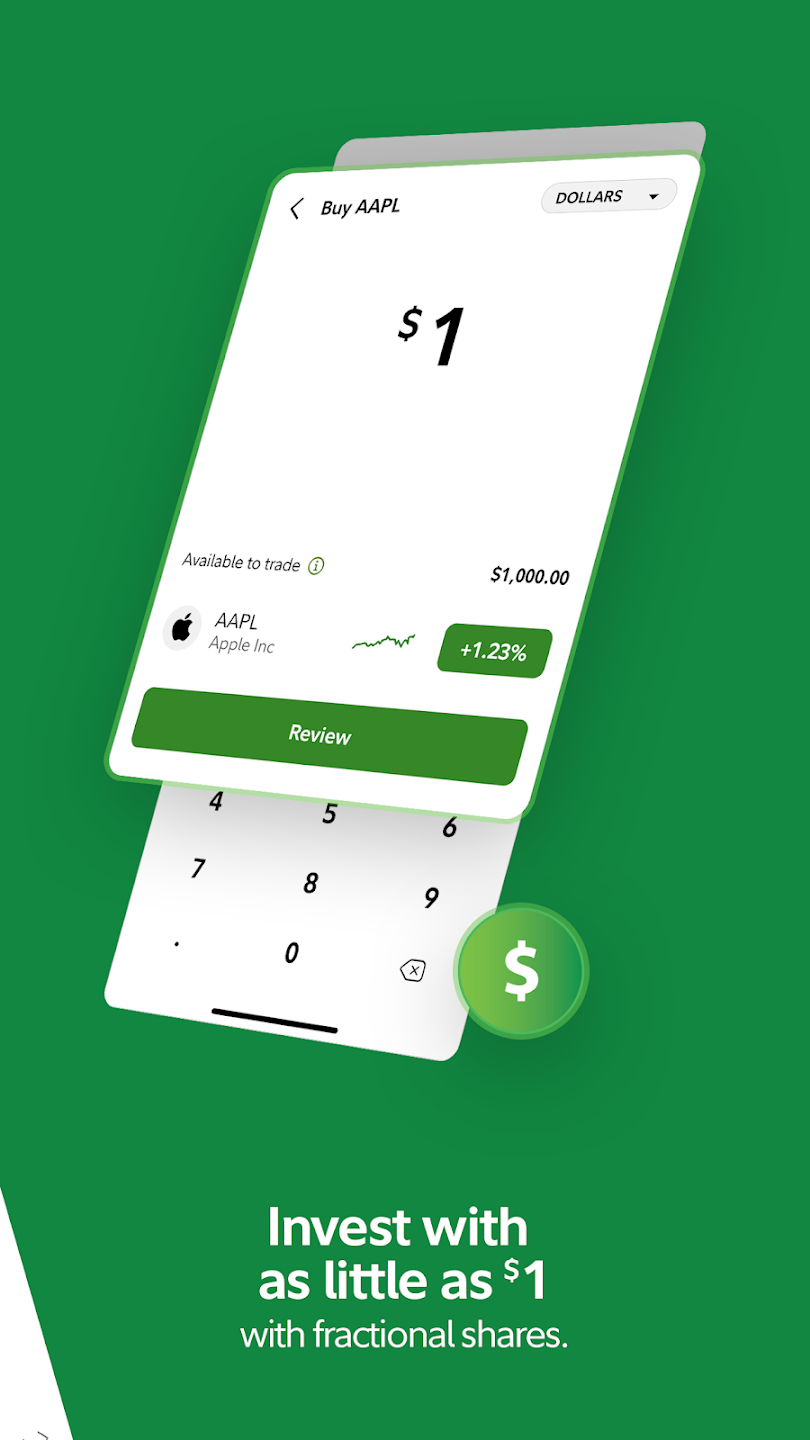

- Stocks by the Slice: This is Fidelity’s fractional share program. If a single share of a major technology company costs $400, a beginner with only $20 can buy a 5% fraction of that share. This feature ensures that small capital constraints do not prevent proper portfolio diversification.

Charles Schwab: Unmatched Client Support and Educational Resources

Following its acquisition of TD Ameritrade, Charles Schwab solidified its position as an industry giant that retains a deeply client-focused approach. Schwab is an ideal choice for beginners who feel overwhelmed by financial terminology and want a guided entry into the market.

- 24/7 Customer Assistance: Schwab provides continuous access to human support staff via phone and live chat. For a beginner worried about making a mistake with their first transfer or trade execution, knowing a licensed professional is available at 3 AM provides significant peace of mind.

- Schwab Starter Kit: New accounts funded with a minimal amount often receive a small cash bonus specifically designated to buy fractional shares of top companies within the S&P 500, giving beginners hands-on experience with institutional equities immediately.

Vanguard: The Pioneer of Passive, Long-Term Index Investing

Vanguard operates under a unique corporate structure where the company is owned by its funds, which are in turn owned by the investors. This structural alignment means Vanguard’s core mission is to keep investment costs as low as possible.

- The Long-Term Philosophy: Vanguard’s digital platform is intentionally less flashy than modern mobile trading apps. It is built to discourage daily, speculative trading and instead promote long-term, passive accumulation.

- Target Retirement Funds: For beginners who want a “set-it-and-forget-it” approach, Vanguard offers premier target-date funds. You select the approximate year you plan to stop working, and the fund automatically adjusts its asset allocation—moving from aggressive stocks to conservative bonds—as you get older.

Robinhood: The Mobile-First Innovation for Casual Micro-Investing

Robinhood fundamentally disrupted the brokerage industry by introducing widespread commission-free trading. It remains a compelling option for younger, digital-native investors who prefer managing their entire lives via a clean mobile interface.

- User Interface Simplicity: The application strips away complex multi-screen trading terminals, making the physical act of purchasing an asset as simple as swiping up on a screen.

- Retirement Incentives: Robinhood has introduced unique incentives for retirement accounts, offering a percentage match on annual contributions to Traditional and Roth IRAs for eligible tiers, which can give a significant boost to a beginner’s retirement balance over time.

Understanding Fractional Shares and Their Impact on Diversification

One of the most revolutionary developments in modern retail investing is the widespread adoption of fractional shares. Historically, high stock prices created an artificial barrier to entry. If an investor had $100 per month to allocate, and a major retail conglomerate traded at $350 per share, the investor could not buy that stock until they saved for four consecutive months.

Fractional shares solve this problem entirely by breaking a single share down into micro-units. The benefits of this feature for a beginner portfolio include:

- Immediate Dollar-Cost Averaging: You can invest a fixed dollar amount every week or month automatically, regardless of whether stock prices are rising or falling. This removes the emotional temptation to “time the market.”

- Instant Portfolio Diversification: Instead of putting your first $100 entirely into one share of a single company, you can allocate $5 to twenty different companies across various sectors (technology, healthcare, energy, consumer goods), immediately lowering your idiosyncratic risk.

- Maximum Capital Utilization: Unused cash balances earn very little when sitting idle. Fractional shares ensure that every single dollar you transfer into your brokerage account goes to work earning returns right away.

The Critical Differences Between Automated Robo-Advisors and Self-Directed Accounts

As you establish your brokerage account, you will face a fundamental strategic choice: Do you want to pick your own investments (Self-Directed), or do you want an algorithm to manage the portfolio for you (Robo-Advisors)?

Self-Directed Investing

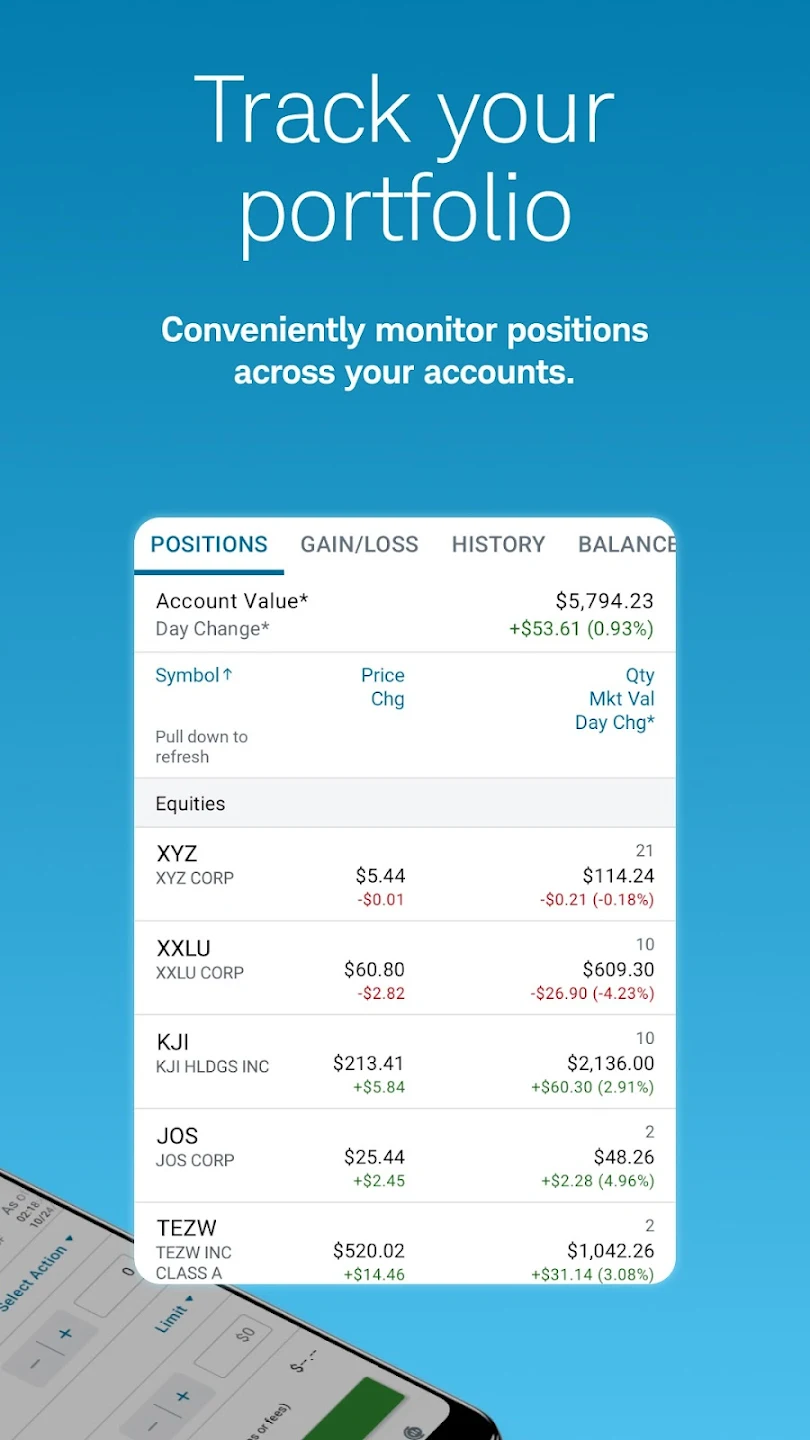

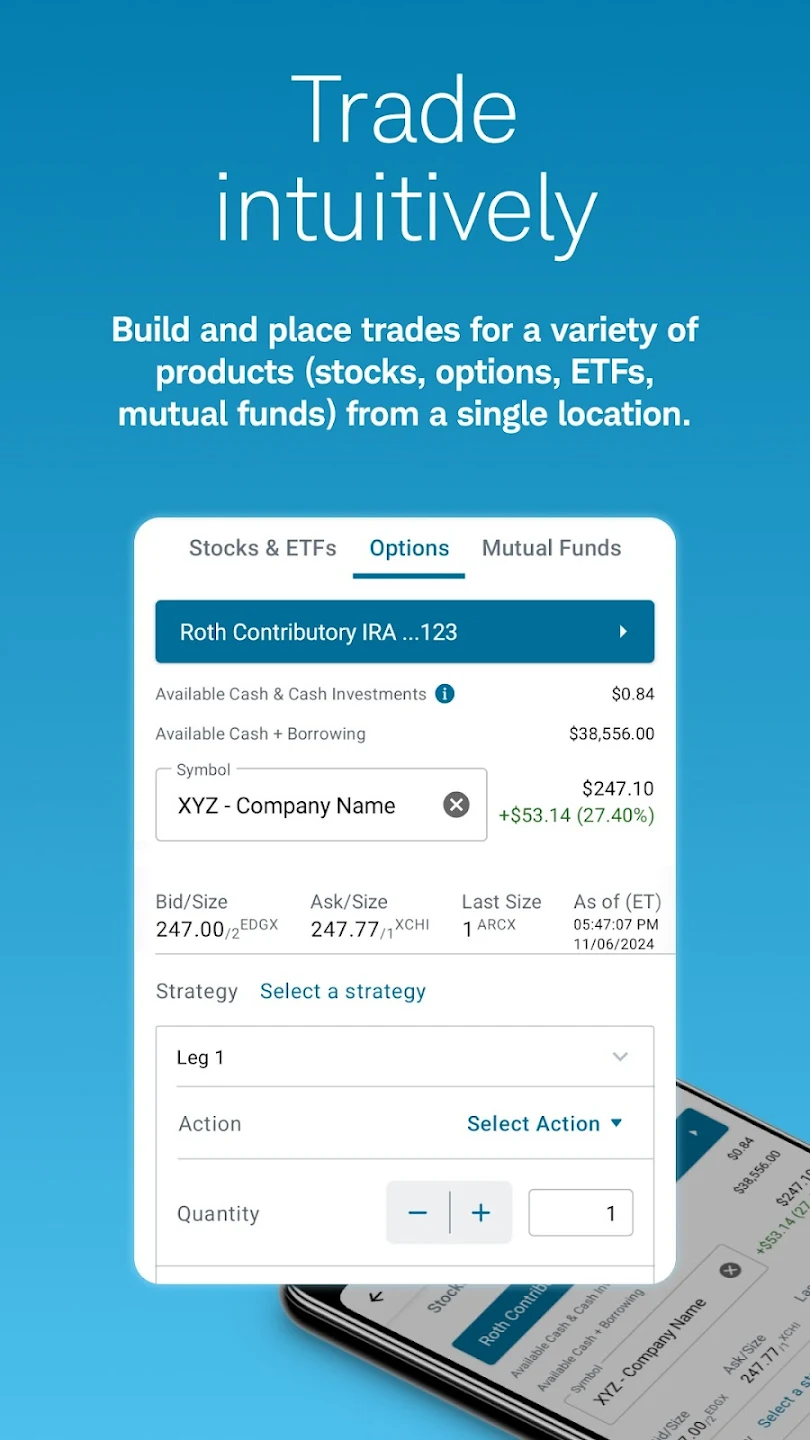

In a self-directed account, you are the portfolio manager. You decide exactly which individual stocks, index funds, or ETFs to purchase. The advantage here is total control and zero management fees. You are not paying anyone to run the account. The drawback is that it requires a baseline level of knowledge and regular portfolio maintenance. You must possess the discipline to rebalance your assets periodically to ensure your risk profile does not drift over time.

Robo-Advisory Management

Platforms like Betterment, Wealthfront, or the automated branches of major brokerages (like Schwab Intelligent Portfolios) utilize automated algorithms to manage your money. When you sign up, you answer a questionnaire regarding your timeline, age, and risk tolerance. The algorithm then constructs a diversified portfolio of low-cost ETFs and automatically handles dividend reinvestment and portfolio rebalancing.

The primary benefit of a robo-advisor is complete automation; it protects beginners from making emotional, panic-driven changes during market downturns. The trade-off is cost. Most robo-advisors charge an annual management fee, typically around 0.25% of your assets under management. While this sounds small, you must evaluate whether that automated management provides enough value to justify the long-term drag on your compounding returns compared to manually buying a total market index fund for free.

Step-by-Step Security Protocol for Opening Your First Investment Account

Once you select the platform that fits your financial strategy, the actual onboarding process is heavily regulated to protect against identity theft and financial fraud. To ensure a smooth account setup, you should approach the registration process systematically.

Step 1: Gathering Regulatory Documentation

Because brokerage firms are subject to strict “Know Your Customer” (KYC) and Anti-Money Laundering (AML) laws, you must verify your identity during setup. You will need to provide your legal name, physical address, date of birth, and a valid government-issued identification number (such as a Social Security Number or Taxpayer Identification Number). You will also be asked about your employment status and annual income to help the broker assess your suitability for specific types of accounts.

Step 2: Choosing the Correct Account Tax Structure

Beginners often confuse the brokerage platform with the account type. A brokerage is simply the house where your accounts live. Inside that house, you can open different types of accounts that feature drastically different tax rules:

- Standard Taxable Brokerage Account: This account offers maximum flexibility. You can deposit money, buy assets, and withdraw funds at any age without penalty. However, you will owe taxes on capital gains whenever you sell an asset for a profit, as well as taxes on dividends received in the calendar year.

- Roth Individual Retirement Account (Roth IRA): Contributions to a Roth IRA are made with after-tax dollars. The massive benefit here is that your investments grow entirely tax-free, and qualified withdrawals in retirement (after age 59½) are completely exempt from income tax. This is often the premier vehicle for young beginners focused on long-term wealth.

- Traditional Individual Retirement Account (Traditional IRA): Contributions here may be tax-deductible in the year you make them, lowering your current taxable income. However, the funds grow tax-deferred, meaning you will pay standard income tax rates on all withdrawals when you retire.

Step 3: Hardening Account Security Infrastructure

Because a brokerage account contains your liquid net worth, it is a high-value target for bad actors. Do not rely on a simple password. Immediately upon account creation, navigate to the settings menu and implement the following protocols:

- Multi-Factor Authentication (MFA): Enable hardware or app-based authentication codes (such as Google Authenticator). Avoid SMS-based text message verification if possible, as it is vulnerable to SIM-swapping scams.

- Biometric Locks:** If utilizing a mobile application, require fingerprint or facial recognition access for every single app launch.

- Trusted Contact Authorization: Specify a trusted family member or advisor whom the brokerage can legally contact if they suspect you are experiencing fraudulent activity or cognitive exploitation.

Moving From Strategy to Action in Your Financial Journey

Selecting the right brokerage is the foundational milestone of your investing life, but the real magic of wealth creation occurs through consistency. The most elegant, high-tech platform is useless if it sits empty. Conversely, a basic, no-frills account can grow into a multi-million dollar nest egg if it is funded systematically month after month.

As you take these first steps, remember that market volatility is a natural feature of capitalism, not a bug. Prices will fluctuate, and downturns will occur. By selecting an institution characterized by low fees, institutional security, and extensive educational depth, you provide your capital with the healthiest possible environment to grow.

The ultimate goal of investing is to shift from a reality where you work exclusively for your money, to a reality where your money works efficiently for you. Choose your platform, automate your regular contributions, focus on diversified index assets, and allow the steady passage of time to handle the rest. Your future financial freedom depends directly on the decisions you make and implement today.