Can You Start Investing in Stocks with $100?

There was a time, not too long ago, when the stock market felt like a private club for the wealthy. If you wanted to buy a share of a major tech giant, you might have needed thousands of dollars just to get through the door. Between high share prices and predatory broker commissions, the “little guy” was often left on the sidelines.

But the world of finance has undergone a massive democratization. Today, the answer to the question “Can you start investing in stocks with $100?” is a resounding yes. In fact, in 2026, $100 is more than enough to build a diversified portfolio that would have made a professional investor jealous thirty years ago.

In this guide, we’ll explore how to turn that $100 bill into a cornerstone for your financial future, the tools you need to use, and why waiting to “have more money” is actually the most expensive mistake you can make.

The Death of the Barrier to Entry: How Fractional Shares Changed Everything

The single biggest reason you can start with $100 today is the rise of fractional shares.

In the past, if a single share of a company like Amazon or Berkshire Hathaway cost $3,000, and you only had $100, you were out of luck. You couldn’t buy 1/30th of a share. You had to save up until you could afford the whole thing.

What are Fractional Shares?

Fractional shares allow you to buy stocks based on the dollar amount you want to spend, rather than the number of shares. If you want to put $10 toward a company whose stock price is $1,000, the brokerage simply grants you 1% of a share.

-

Diversification: With $100, you can now own pieces of 10 different companies for $10 each.

-

Accessibility: No stock is “too expensive” for your budget.

-

Dividends: You still receive dividends! If a company pays a $1 dividend per full share, and you own 10% of a share, you get $0.10.

This shift has turned the stock market from a “pay-to-play” arena into a “start-where-you-are” opportunity.

The Power of Compounding: Why $100 Today is Better than $1,000 Later

Many people wait until they have a “significant” amount to invest. They think, “What is $100 going to do?” The reality is that time is a much more powerful factor in wealth creation than the initial deposit.

The Math of Starting Early

Let’s look at the power of compound interest. If you invest $100 and it grows at an average annual rate of 8%, that money doubles roughly every nine years.

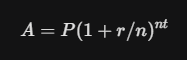

The formula for compound interest is:

Where:

-

A = the future value of the investment

-

P = the principal investment ($100)

-

r = the annual interest rate (0.08)

-

t = the number of years the money is invested

If you are 20 years old and invest $100, by the time you are 65, that single $100 will have grown to over **$3,000** without you ever adding another penny. If you wait until you are 40 to start, that same $100 only grows to about **$700**. The “cost” of waiting twenty years was $2,300 on a tiny $100 investment. Now imagine that scale with $100 every month!

Stocks vs. ETFs: Where Should Your First $100 Go?

When you have $100, you have two primary paths: buying individual stocks or buying Exchange-Traded Funds (ETFs).

Individual Stocks (High Risk, High Reward)

Buying a single company like Apple, Tesla, or Coca-Cola means your $100 is tied to the success of that specific business.

-

Pros: If the company “moons” (grows rapidly), your $100 can turn into $500 quickly.

-

Cons: If the company faces a scandal or bankruptcy, you could lose everything.

ETFs (The Smart Beginner Choice)

An ETF is a “basket” of hundreds or thousands of stocks. When you buy one share of an S&P 500 ETF (like VOO or SPY), your $100 is instantly spread across the 500 largest companies in the United States.

-

Pros: Built-in diversification. If one company in the 500 fails, the other 499 carry the load.

-

Cons: You won’t see “overnight” riches, but you will see steady, long-term growth.

Expert Recommendation: For your first $100, a broad-market ETF is almost always the better choice. It provides a “safety net” while you learn the ropes.

Choosing the Best Brokerage for Small Accounts

Not all brokerages are friendly to $100 investors. To keep your $100 working for you and not for a bank, you need to look for three specific features:

-

Zero Commissions: Never pay a fee to buy or sell a stock. If a broker charges $5 per trade, you lose 5% of your $100 the moment you click “Buy.”

-

No Account Minimums: Some “old school” firms require $1,000 to open an account. Avoid these.

-

Fractional Share Support: As discussed, this is mandatory for a $100 budget.

Popular 2026 Options

-

Robinhood/Webull: Great for user experience and fractional shares.

-

Fidelity/Charles Schwab: Excellent for long-term investors who want high-quality research tools alongside zero fees.

-

Vanguard: The king of low-cost ETFs, though their app interface is more traditional.

Risk Management: How to Not Lose Your $100 in a Week

Investing is not gambling, but many beginners treat it that way. To protect your $100, follow these ground rules:

Avoid Penny Stocks

Penny stocks (companies trading for less than $5) look attractive because you can buy “thousands” of shares with $100. Don’t do it. These stocks are often highly manipulated, volatile, and lack financial transparency. It is better to own 0.05% of a world-class company than 10,000 shares of a dying one.

Don’t “Day Trade”

Buying and selling within minutes or hours is a recipe for losing money. For a $100 investor, your greatest edge is your holding period. Buy a piece of a great business or fund and plan to hold it for at least five years.

Understand Volatility

The stock market moves in waves. Your $100 might become $90 next week. That is not a “loss” unless you sell. It is simply the market breathing. Stick to your plan.

The “DCA” Strategy: Turning $100 into a Fortune

If you only ever invest $100 once, you’ll have a nice dinner fund in thirty years. But if you use that $100 as the start of a Dollar Cost Averaging (DCA) strategy, you can change your life.

How DCA Works

DCA is the practice of investing a fixed amount of money at regular intervals, regardless of the price.

-

If the market is up: Your $100 buys fewer shares.

-

If the market is down: Your $100 buys more shares (you’re buying the “sale”).

By automating $100 a month into an S&P 500 ETF, you remove the emotion from investing. You aren’t “timing” the market; you are “time-in” the market. Over 30 years at an 8% return, $100 a month turns into approximately **$150,000**. That is a significant return on a habit that costs less than a weekly takeout order.

The Hidden Costs: Taxes and Inflation

Even with $100, you need to be aware of the “wealth eroders.”

Inflation: The Reason You MUST Invest

If you keep your $100 under your mattress, inflation (the rising cost of goods) will eat its value. In 10 years, that $100 will buy significantly less than it does today. Investing is the only reliable way to keep your purchasing power ahead of inflation.

Taxes on Dividends and Gains

When you make money in the stock market, the government wants a piece.

-

Capital Gains Tax: You only pay this when you sell for a profit.

-

Dividend Tax: You pay this on the cash payments you receive, even if you reinvest them.

-

Tip: If you are in the U.S., consider starting with a Roth IRA. In a Roth, your $100 grows tax-free, and you pay zero taxes when you withdraw it in retirement.

Comparing Investment Paths for $100

| Strategy | Risk Level | Potential Return | Effort Level |

| S&P 500 ETF | Moderate | 7–10% annually | Low (Set and forget) |

| Dividend Aristocrats | Low/Moderate | 6–8% + Dividends | Medium (Pick safe companies) |

| Individual Tech Stocks | High | 15%+ or -50% | High (Requires research) |

| Savings Account | Zero | 0.5–4% | Low (But loses to inflation) |

The Psychological Benefit of Starting Small

The most important reason to start with $100 is not the money—it’s the education.

When you have $100 on the line, you start paying attention. You read the news differently. You learn what a “P/E ratio” is. You learn how you react when the market drops 2%.

Learning these lessons with $100 is “cheap” tuition. If you wait until you have $50,000 to start, your first mistake will cost you thousands. Making your first mistake with $100 only costs you a few dollars.

Stop Planning and Start Buying

Can you start investing in stocks with $100? Absolutely. In fact, $100 is the perfect amount to break the seal of “analysis paralysis.”

The market doesn’t care if you are a millionaire or a student starting with $100; it rewards everyone who has the discipline to stay invested for the long haul. Open a brokerage account, buy $100 of a diversified ETF, and officially join the ranks of the world’s investors. Your future self will thank you for the $100 you spent today.