How Much Can You Borrow Based on Your Income?

When you decide it’s time to make a major life purchase—whether it’s buying a home, upgrading your car, or consolidating high-interest debt—the first question that usually comes to mind is: “How much will the bank actually give me?”

While it is tempting to focus solely on your annual salary, lenders look at your financial profile through a much more complex lens. Your income is the engine, but your existing debts, credit history, and the current economic climate of 2026 are the brakes. Understanding the relationship between your paycheck and your borrowing capacity is the key to getting approved without overextending yourself.

In this guide, we will explore the mathematical formulas lenders use, the “rules of thumb” for different loan types, and how you can maximize your borrowing power while staying financially secure.

The Golden Metric: Understanding the Debt-to-Income (DTI) Ratio

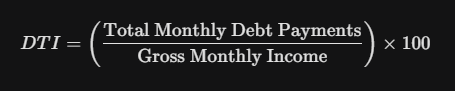

If there is one number that determines your borrowing fate, it is the Debt-to-Income (DTI) ratio. Lenders use this to measure your ability to manage monthly payments and repay the money you plan to borrow.

In simple terms, your DTI ratio is the percentage of your gross monthly income that goes toward paying your fixed monthly debts. Most lenders in 2026 follow strict guidelines regarding this ratio to ensure you aren’t “house poor” or buried under personal loan payments.

The DTI Formula

To calculate your current standing, use the following formula:

What Qualifies as “Debt” in this Equation?

-

Monthly mortgage or rent payments.

-

Car loan installments.

-

Minimum credit card payments.

-

Student loan payments.

-

Alimony or child support.

-

Other personal or installment loans.

Note: Living expenses like groceries, utilities, and insurance are generally not included in the DTI calculation, though lenders expect you to have enough “residual income” to cover them.

The 28/36 Rule: The Standard Benchmark for Borrowing Limits

For decades, the 28/36 rule has been the “North Star” for financial advisors and mortgage lenders. Although some modern online lenders allow for higher ratios, staying within these bounds is the safest way to ensure long-term stability.

1. The Front-End Ratio (28%)

This rule suggests that you should spend no more than 28% of your gross monthly income on housing-related expenses. This includes your principal, interest, taxes, and insurance (often abbreviated as PITI).

2. The Back-End Ratio (36%)

This rule states that your total debt—including your new house payment plus all other recurring debts—should not exceed 36% of your gross monthly income.

Why Lenders Push the Limits in 2026

In high-cost-of-living areas, many lenders have increased the acceptable back-end DTI to 43% or even 50% for borrowers with high credit scores. However, just because a bank will lend you that much doesn’t mean you should take it. Borrowing at a 50% DTI leaves almost no room for emergencies or changes in income.

Gross Income vs. Net Income: Why Lenders Use the “Wrong” Number

One of the most confusing aspects of borrowing for a layperson is why banks use Gross Monthly Income (before taxes) rather than Net Income (take-home pay).

Lenders use gross income because it is a standardized, verifiable figure that doesn’t fluctuate based on your specific tax deductions, 401(k) contributions, or health insurance premiums. However, from a personal budgeting perspective, relying on gross income is dangerous.

The Reality Check

If you earn $10,000 a month gross, but your take-home pay after taxes and benefits is $7,000, a “safe” 36% DTI based on gross income ($3,600) actually represents over 50% of your take-home pay. Before signing any loan document, always run the numbers against your actual bank balance, not just the number on your tax return.

How Much Can You Borrow for a Mortgage Based on Income?

Mortgages are the most common form of long-term leverage. Because the loan is secured by the property, banks are willing to lend much larger multiples of your income than they would for an unsecured personal loan.

The Income Multiplier Method

A common (though simplified) way to estimate mortgage capacity is the income multiplier. Generally, most people can qualify for a mortgage that is 3 to 5 times their annual gross salary.

-

Annual Income $50,000: Estimated Max Loan $150,000 – $250,000.

-

Annual Income $100,000: Estimated Max Loan $300,000 – $500,000.

-

Annual Income $200,000: Estimated Max Loan $600,000 – $1,000,000.

Factors That Change the Multiplier:

-

Interest Rates: In 2026, if interest rates are high, your “buying power” decreases because more of your monthly payment goes to interest rather than the loan principal.

-

Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, often making lenders more comfortable with higher income multiples.

-

Property Taxes: In states with high property taxes, your borrowing capacity will be lower because the “T” in PITI is higher.

Personal Loan Limits: How Unsecured Debt is Calculated

Personal loans are typically unsecured, meaning there is no collateral (like a house or car) for the bank to seize if you stop paying. Consequently, the borrowing limits are much stricter and more closely tied to your monthly surplus.

Most personal loan lenders cap their maximum loan amounts at around $50,000 to $100,000, regardless of how much you earn. To qualify for the maximum, lenders usually look for:

-

A DTI ratio below 35%.

-

A stable employment history (usually 2+ years).

-

A “High” or “Exceptional” credit score.

If you earn $120,000 a year ($10k/month) and have $2,000 in existing monthly debt, a lender might approve you for a personal loan payment of up to $1,500, which could translate to a $60,000 loan over 5 years, depending on the interest rate.

Auto Loans and the 10% Rule: Avoiding the “Car Poor” Trap

Car loans are unique because vehicles are depreciating assets. Lenders are often more lenient with auto loan approvals, but financial experts recommend much stricter limits than what the bank might allow.

The 10% Rule for Auto Loans

To maintain a healthy financial life, your total car-related expenses (payment, insurance, and fuel) should not exceed 10% to 15% of your take-home pay.

If you take a loan based on your gross income limits, you might find yourself with a shiny new car but no money for maintenance or insurance. Furthermore, most auto lenders will not approve a loan where the monthly payment exceeds 15-20% of your gross monthly income.

How Credit Scores Influence Your Total Borrowing Power

Your income sets the ceiling for how much you can borrow, but your credit score determines the cost of that borrowing.

Because a higher credit score results in a lower interest rate, it effectively increases the amount of principal you can afford with the same monthly payment.

Example: The “Interest Rate” Effect

Imagine you have $1,000 a month available for a 30-year mortgage payment (Principal & Interest only):

-

With a 4% Interest Rate: You can borrow approximately $210,000.

-

With a 7% Interest Rate: You can borrow approximately $150,000.

By improving your credit score, you can “borrow” an extra $60,000 without earning a single extra penny in salary. This is why credit repair is often the fastest way to increase your borrowing capacity.

Borrowing for the Self-Employed and Gig Workers in 2026

If you are a freelancer, business owner, or gig worker, calculating your borrowing power is slightly different. Lenders don’t look at your “top-line” revenue; they look at your Adjusted Gross Income (AGI) from your tax returns.

The 2-Year Rule

Most lenders require at least two years of consistent tax returns to prove stability.

The Catch: Many self-employed individuals use legal tax deductions to lower their taxable income. While this saves you money in April, it reduces your “income” in the eyes of a lender. If you plan to borrow a large sum in the next year, you may need to work with a CPA to balance your tax deductions against your need for “verifiable income.”

Residual Income: The “Secret” Metric Lenders Use

Some lenders, particularly those issuing VA loans or high-balance personal loans, use a metric called Residual Income. Instead of looking at a percentage (DTI), they look at the actual dollar amount you have left over at the end of the month after all debts and estimated living expenses (utilities, food) are paid.

In 2026, with the cost of living rising in many urban centers, having a $2,000+ monthly “buffer” is often more important to a lender than a specific DTI percentage. If your income is high but your lifestyle expenses are also massive, the bank may limit your borrowing to ensure you don’t default at the first sign of inflation.

Strategies to Increase Your Borrowing Capacity

If you’ve run the numbers and realized you can’t borrow as much as you need, there are several levers you can pull:

-

Pay Down Existing Debt: Reducing a $300/month car payment has a much larger impact on your borrowing power than a small raise at work.

-

Add a Co-Borrower: Adding a spouse or partner’s income can drastically lower your DTI and increase the total loan amount.

-

Extend the Loan Term: Moving from a 15-year to a 30-year mortgage (or a 3-year to a 5-year personal loan) lowers the monthly payment, allowing you to borrow more principal (though you will pay more in total interest).

-

Wait for Interest Rates to Drop: As rates fall, your monthly payment covers more principal.

-

Check for Errors on Your Credit Report: A mistake that lowers your score could be costing you tens of thousands in borrowing capacity.

The Danger of “Borrowing to the Max”

Just because a lender says you can borrow $500,000 doesn’t mean it’s a good idea. Lenders are in the business of selling debt; they are not your financial planners.

The “House Poor” Scenario

When you borrow to the absolute limit of your DTI, you are one “bad month” away from a crisis. If your water heater breaks, your car needs new tires, or you have a medical copay, a 45% DTI ratio can lead to credit card debt just to survive.

The Pro Tip: Aim to keep your actual debt payments under 25% of your net (take-home) income, regardless of what the bank’s computer says. This creates a “peace of mind” buffer that allows for travel, savings, and investment.

Knowing Your Numbers is the Best Defense

Your income is the foundation of your borrowing power, but the “math” of lending in 2026 is multifaceted. By understanding your DTI ratio, the 28/36 rule, and the impact of interest rates on your principal, you can walk into a bank or apply online with total confidence.

Before you apply, take the time to calculate your own limits. Use your gross income for the bank’s application, but use your net income for your own heart and mind. Borrowing smart isn’t about getting the most money possible—it’s about getting the right amount of money at a cost you can truly afford.

Quick Reference: Borrowing Capacity Table

| Income (Annual Gross) | Monthly Gross | Estimated Max Monthly Debt (36% DTI) | Estimated Mortgage Capacity (4x Multiplier) |

| $40,000 | $3,333 | $1,200 | $160,000 |

| $60,000 | $5,000 | $1,800 | $240,000 |

| $80,000 | $6,666 | $2,400 | $320,000 |

| $100,000 | $8,333 | $3,000 | $400,000 |

| $150,000 | $12,500 | $4,500 | $600,000 |