How to create an investment portfolio for retirement

Retirement is no longer just a destination reached at age 65; it is a financial state of being where your assets generate enough income to support your lifestyle indefinitely. However, the path to that freedom isn’t paved with luck—it is built through a deliberate, structured investment portfolio.

For many, the idea of “investing for retirement” feels like staring into a cockpit of a jet—full of confusing buttons, flashing lights, and jargon that seems designed to gatekeep wealth. The truth is far simpler: retirement investing is a marathon of consistency and asset allocation.

In this guide, we will peel back the layers of complexity to show you exactly how to build a portfolio that stands the test of time, survives market volatility, and ultimately buys back your freedom.

Defining Your Retirement Vision and Time Horizon

Before you pick a single stock or bond, you must determine your destination. A retirement portfolio for a 22-year-old looks nothing like a portfolio for someone at age 55.

The Power of the Time Horizon

Your “time horizon” is the number of years between now and when you need to start withdrawing money. This is the most critical factor in your strategy.

-

Long Horizon (20+ years): You can afford to be aggressive. Market crashes are merely “sales” where you can buy more shares at a discount because you have decades for the market to recover.

-

Short Horizon (Less than 10 years): You must prioritize capital preservation. A 30% market drop right before retirement can be devastating if you don’t have enough stable assets to weather the storm.

Estimating Your Retirement Number

A common rule of thumb is the 25x Rule. To maintain your current lifestyle, you should aim to save 25 times your annual expenses. If you plan to spend $50,000 a year, your target is $1.25 million.

Assessing Risk Tolerance vs. Risk Capacity

One of the biggest mistakes investors make is confusing how much risk they want to take with how much risk they can take.

-

Risk Tolerance: This is your psychological ability to handle a market drop. If seeing your account balance dip by 10% makes you lose sleep or want to sell everything, you have a low risk tolerance.

-

Risk Capacity: This is your mathematical ability to take a hit. Even if you have a high tolerance, if you are retiring in two years, your capacity for risk is low because you don’t have time to recover from a crash.

A balanced portfolio aligns these two. If they are out of sync—for example, if you are aggressive but panic easily—you are likely to sell at the bottom, which is the fastest way to destroy wealth.

The Pillars of Asset Allocation: Stocks, Bonds, and Cash

Asset allocation is the process of dividing your money among different types of investments. Statistics show that over 90% of a portfolio’s returns are determined by asset allocation, rather than the specific stocks you choose.

Equities (Stocks)

Stocks represent ownership in companies. They are the engine of growth in your retirement portfolio. While they are volatile in the short term, they have historically provided the highest long-term returns, averaging around 7–10% annually before inflation.

Fixed Income (Bonds)

Bonds are essentially loans you make to governments or corporations. In exchange, they pay you interest. Bonds act as the “ballast” on your ship; they don’t grow as fast as stocks, but they provide stability when the stock market gets choppy.

Cash and Equivalents

This includes high-yield savings accounts, money market funds, and certificates of deposit (CDs). These offer the lowest returns but provide immediate liquidity and safety.

| Age Group | Suggested Stock % | Suggested Bond % |

| 20s – 30s | 80% – 90% | 10% – 20% |

| 40s | 70% – 80% | 20% – 30% |

| 50s | 60% – 70% | 30% – 40% |

| At Retirement | 40% – 60% | 40% – 60% |

Diversification: Your Only “Free Lunch” in Finance

Diversification is the practice of spreading your investments across various sectors, industries, and geographies so that a failure in one area doesn’t sink your entire portfolio.

Beyond Large-Cap Stocks

Many investors only buy big, well-known companies (like Apple or Amazon). A truly diversified retirement portfolio should include:

-

Small-Cap Stocks: Smaller companies with high growth potential.

-

International Markets: Developed markets (Europe, Japan) and Emerging markets (India, Brazil) to capture global growth.

-

Real Estate (REITs): Real Estate Investment Trusts allow you to own property without being a landlord.

By diversifying, you ensure that you aren’t over-exposed to a single country’s economy or a single industry’s downturn.

Maximizing Tax-Advantaged Retirement Accounts

In the journey to retirement, taxes are a significant “drag” on your returns. To combat this, you should utilize accounts specifically designed for retirement savings.

Employer-Sponsored Plans (401(k) / 403(b))

If your employer offers a “match,” this is a 100% return on your investment instantly. Always contribute enough to get the full match before investing elsewhere. These accounts allow you to contribute pre-tax dollars, reducing your taxable income today.

Individual Retirement Accounts (IRA)

-

Traditional IRA: Contributions are often tax-deductible, but you pay taxes when you withdraw the money in retirement.

-

Roth IRA: You pay taxes upfront, but the money grows tax-free, and your withdrawals in retirement are also tax-free. This is incredibly powerful for young investors who expect to be in a higher tax bracket later in life.

The Health Savings Account (HSA)

Often called the “secret retirement account,” the HSA offers a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for medical expenses are tax-free. After age 65, it can be used for any expense (though you’ll pay income tax, similar to a Traditional IRA).

The Strategy of Low-Cost Index Funds and ETFs

You don’t need to be a “stock picker” to retire wealthy. In fact, most professional fund managers fail to beat the market over long periods.

Why Index Funds Win

An index fund (or ETF) tracks a specific market index, like the S&P 500. Instead of trying to find the “next big thing,” you simply buy the entire market.

-

Low Fees: Active funds often charge 1% or more in fees. Many index funds charge less than 0.05%.

-

Consistency: You get the average return of the market, which, over decades, is a winning strategy.

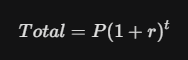

Consider the impact of a 1% fee over 30 years on a $100,000 portfolio growing at 7%:

Without fees, you’d have roughly $761,225. With a 1% fee (reducing growth to 6%), you’d have $574,349. That 1% fee cost you nearly $187,000!

Rebalancing: Staying True to Your Strategy

As the market fluctuates, your original asset allocation will shift. If stocks perform well, your 80/20 portfolio might become 90/10. This means you are now taking more risk than you intended.

How to Rebalance

Once or twice a year, you should “rebalance” your portfolio. This involves selling a portion of the assets that have grown too large and buying more of the assets that have underperformed.

Note: Rebalancing is a disciplined way to “sell high and buy low.” It feels counterintuitive to sell your winners, but it is the best way to maintain your risk profile.

Managing Inflation and Purchasing Power

One of the quietest threats to retirement is inflation. If the cost of living doubles every 20 years, your $1 million might only buy half as much when you actually need it.

To protect against inflation, your portfolio must have “inflation hedges”:

-

Stocks: Companies can raise prices as their costs go up, often keeping pace with inflation.

-

TIPS (Treasury Inflation-Protected Securities): These are government bonds specifically designed to increase in value as inflation rises.

-

Real Estate: Rents typically rise along with inflation.

Transitioning from Accumulation to Distribution

As you reach the “Finish Line,” your focus shifts from growing your money to making it last. This is where the 4% Rule comes into play.

The 4% Rule suggests that if you withdraw 4% of your portfolio in your first year of retirement and adjust for inflation each year after, your money has a high probability of lasting 30 years. However, this depends on a balanced portfolio. If you are 100% in cash, inflation will eat your savings. If you are 100% in stocks, a single market crash early in retirement could drain your account.

The Cash Bucket Strategy

Many retirees keep 2–3 years of living expenses in cash or “cash equivalents.” This way, if the stock market crashes, they don’t have to sell their stocks at a loss to pay for groceries; they just live off their “cash bucket” until the market recovers.

Common Pitfalls to Avoid in Retirement Investing

Building a portfolio is as much about what you don’t do as what you do.

-

Chasing Performance: Don’t buy an investment just because it did well last year. Winners rotate.

-

Emotional Reactivity: The market will crash. Multiple times. The only people who get hurt on a roller coaster are the ones who jump off while it’s moving.

-

Lifestyle Creep: As your income grows, try to keep your expenses stable. The more you save now, the sooner your portfolio can support you.

-

Waiting to Start: Because of compound interest, waiting 5 or 10 years to start can cost you hundreds of thousands of dollars in the long run.

Your Freedom is Within Reach

Creating a retirement portfolio isn’t a “set it and forget it” event, but it doesn’t have to be a full-time job either. By choosing a balanced asset allocation, utilizing tax-advantaged accounts, and staying disciplined through market cycles, you are building a machine that will eventually work so you don’t have to.

The best time to start was ten years ago. The second best time is today.