How Young Adults Can Start Investing Early

If you are in your 20s or early 30s, you possess a financial asset that even the wealthiest billionaires on Earth cannot buy more of: Time.

While many young adults feel that investing is something to “figure out later” once they have a “real job” or a mortgage, the reality is that waiting even five years to start can cost you hundreds of thousands of dollars in potential wealth. Investing isn’t just for the suits on Wall Street; it is a tool for anyone who wants to stop trading their time for money and start letting their money work for them.

In this comprehensive guide, we will break down exactly how you can start investing today, even with a small budget, and why starting early is the single most important decision you will ever make for your future self.

The Superpower of Youth: Understanding Time Value and Compounding

The reason young adults have such a massive advantage is a mathematical phenomenon known as Compound Interest. When you invest, you earn a return on your initial money. The following year, you earn a return on that original money plus the returns from the year before.

Over short periods, this looks like a small snowball. Over 30 or 40 years, it becomes an avalanche.

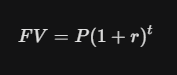

The Mathematics of Starting Early

Let’s look at the formula for future value ($FV$) to see how time ($t$) acts as an exponent, meaning its impact is non-linear:

Where:

-

P = Principal (your initial investment)

-

r = Annual interest rate

-

t = Time in years

If you invest $300 a month starting at age 20, assuming an 8% average annual return, you would have approximately $1.58 million by age 65.

If you wait until age 30 to start investing that same $300 a month, you would end up with roughly $680,000.

The Cost of Waiting: By waiting just 10 years, you lose nearly $900,000 in potential wealth, even though you only “saved” $36,000 in contributions during that decade.

Phase 1: Building a Rock-Solid Financial Foundation

Before you buy your first stock or ETF, you must ensure your financial “house” is in order. Investing while your foundation is shaky is like building a skyscraper on sand.

1. Eliminate High-Interest Debt

Not all debt is created equal. A mortgage might have a 6% interest rate, but credit card debt often carries rates of 20% to 30%. If you invest in the stock market expecting an 8% return while paying 25% interest on a credit card, you are effectively losing 17% of your wealth every year.

-

The Rule: Pay off any debt with an interest rate higher than 7% before investing aggressively.

2. Build an Emergency Fund

The stock market is volatile. If you invest your rent money and the market drops 10% the next day, you’re in trouble.

-

Aim to save 3 to 6 months of essential living expenses in a high-yield savings account (HYSA). This ensures you never have to sell your investments at a loss just to cover an unexpected car repair or medical bill.

3. Define Your “Why”

Are you investing for retirement? A house down payment in five years? Financial independence (FIRE)? Your goals will dictate your Asset Allocation—how much risk you should take.

Phase 2: Decoding Investment Vehicles (Where to Put Your Money)

For young adults, the “where” is often as important as the “how much.” In the United States and many other regions, the government provides special accounts to encourage people to save for the future.

The “Big Three” Accounts for Young Investors

| Account Type | Tax Benefit | Best For |

| 401(k) / 403(b) | Pre-tax contributions (lowers today’s taxes) | Employer matching (Free Money!) |

| Roth IRA | Tax-free growth and withdrawals | Long-term wealth for young earners |

| Brokerage Account | None (fully taxable) | Flexibility and mid-term goals |

Why the Roth IRA is a Young Adult’s Best Friend

A Roth IRA is particularly powerful for those early in their careers. You contribute money that has already been taxed. In exchange, the government allows that money to grow for decades, and when you withdraw it at age 59.5, you pay zero capital gains tax. For a young person whose tax bracket is likely lower now than it will be in the future, this is an incredible deal.

Phase 3: Choosing Your First Investments (Keep It Simple)

The biggest mistake beginners make is overcomplicating their portfolio. You do not need to find the “next Tesla” to become a millionaire. You just need to own the market.

1. Index Funds and ETFs

An Index Fund is a basket of stocks that tracks a specific part of the market, like the S&P 500 (the 500 largest US companies).

-

Why they win: They are low-cost, diversified, and historically outperform most professional stock pickers.

-

ETFs (Exchange-Traded Funds): These are like index funds but trade like stocks, making them easy to buy with small amounts of money.

2. Target Date Funds (TDFs)

If you want a “set it and forget it” option, TDFs are perfect. You pick the year you plan to retire (e.g., “Target Date 2060”), and the fund automatically adjusts its risk. It starts aggressive (mostly stocks) while you are young and becomes conservative (more bonds) as you get older.

3. Fractional Shares

Don’t have $400 to buy one share of a major tech stock? Many modern brokerages allow you to buy fractional shares. You can invest as little as $1 or $5 into any company you believe in.

Phase 4: The Step-by-Step Action Plan to Start Today

Follow these steps to go from $0 to an active investor in less than 30 minutes.

Step 1: Open an Account

Choose a reputable, low-fee brokerage. In the US, companies like Fidelity, Vanguard, and Charles Schwab are the “big three” for a reason—they offer robust tools and $0 commission trades. For a more mobile-friendly experience, apps like Betterment or Wealthfront offer automated “Robo-Advising.”

Step 2: Set Up an Automatic Transfer

Consistency beats intensity. Set up an automatic transfer from your checking account to your investment account for the day after you get paid. Whether it is $50 or $500, making it automatic removes the temptation to spend that money elsewhere.

Step 3: Buy a Diversified Fund

Once the money is in your account, you have to actually buy something. A popular “starter” investment is a Total Stock Market Index ETF (like VTI or ITOT). This gives you a tiny piece of every publicly traded company in the country.

Phase 5: Navigating the Psychology of Investing

Your greatest enemy as an investor isn’t the market; it’s your own brain. Young adults are often more susceptible to “hype” cycles.

1. Ignore the Noise (FOMO vs. Fundamentals)

Social media is full of people claiming to have made millions on a specific “meme stock” or a new cryptocurrency. While some get lucky, many more lose everything.

-

The Strategy: Treat 90% of your portfolio as “boring” long-term investments. If you want to speculate on high-risk assets, do it with only 5% to 10% of your money—an amount you are prepared to lose.

2. Embrace Volatility

Market “corrections” (when the market drops 10% or more) happen roughly once a year on average. For a 25-year-old, a market crash is actually good news. It means you can buy more shares at a discount.

Remember: You only lose money in the stock market if you sell. If you hold through the downturn, your “paper loss” remains just that—on paper.

Advanced SEO Techniques: Expanding Your Knowledge Base

To truly master your finances, you should understand a few more advanced concepts that will help your portfolio grow efficiently.

Expense Ratios: The Hidden Wealth Killer

Every fund you buy has an Expense Ratio (a management fee). A 1% fee might sound small, but over 30 years, it can eat up nearly 25% of your total wealth.

-

Target: Look for index funds with expense ratios below 0.10%.

Dollar-Cost Averaging (DCA)

By investing a fixed amount every month, you naturally buy more shares when prices are low and fewer when prices are high. This lowers your average cost over time and prevents you from trying to “time the market,” which is a losing game for almost everyone.

Asset Rebalancing

Once a year, check your portfolio. if your stocks have performed so well that they now make up 95% of your portfolio instead of your intended 80%, you may want to sell a little and move it into other assets to maintain your desired risk level.

The “Lifestyle” of a Successful Young Investor

Investing isn’t just about what happens in your brokerage account; it’s about your relationship with money.

-

Audit Your Subscriptions: Are you paying for four streaming services you don’t watch? Redirecting $30 a month into your Roth IRA could result in an extra $50,000 in retirement.

-

Invest in Your Earning Power: The more you earn, the more you can invest. Spending money on a certification, a book, or a seminar that increases your salary is often the best “investment” you can make in your 20s.

-

The Power of “No”: It is okay to skip the expensive group trip or the brand-new car to fund your future. You are trading a temporary luxury today for permanent freedom tomorrow.

Your Future Self is Counting on You

The journey to wealth doesn’t require a genius-level IQ or a massive inheritance. It requires the discipline to start small, the patience to wait, and the wisdom to keep things simple.

As a young adult, you have the ultimate advantage. Don’t let the fear of “not knowing enough” or “not having enough” paralyze you. The stock market is the greatest wealth-creation machine in human history, and it is open for business.

Open that account, set up that $25 monthly transfer, and plant the seed today. In thirty years, you won’t remember the $25 you missed each month, but you will certainly cherish the forest of wealth that grew because you had the courage to start early.