Learn how to avoid impulse purchases

We have all been there. You are scrolling through your favorite social media app, browsing an online marketplace, or simply walking down the aisle of a local store when suddenly, an item catches your eye. It looks perfect. A wave of excitement hits you, and before your logical brain can intervene, you hear the familiar chime of your credit card being swiped or see the “Order Confirmed” screen pop up on your phone.

In the moment, it feels great. But a few hours or days later, that initial rush of excitement fades, leaving behind a familiar sensation: buyer’s remorse.

Impulse purchases are one of the single greatest threats to your long-term financial health. They act as silent leaks in your monthly budget, quietly draining cash that could otherwise be used to pay off debt, build an emergency fund, or invest for your future. Retailers spend billions of dollars studying consumer psychology to design environments, advertisements, and digital checkout pipelines explicitly engineered to make you spend money without thinking.

If you are wondering how to stop impulse buying and save money, you are taking a massive step toward financial freedom. Overcoming this habit isn’t about depriving yourself of joy; it is about shifting from accidental, emotional spending to intentional, purposeful wealth building.

This comprehensive guide breaks down the underlying psychology of impulse buying and provides actionable, step-by-step psychological hacks and financial habits to help you break the cycle for good.

The Psychology Behind Impulse Buying: Why Your Brain Loves Sudden Shopping Spies

To successfully defeat a bad financial habit, you must first understand the underlying root cause. Impulse buying is rarely a structural problem of logic or math; it is a complex psychological response driven by your brain’s chemistry.

The Dopamine Loop

When you discover a new item or see a limited-time sale banner, your brain releases a surge of dopamine—the chemical messenger responsible for pleasure, motivation, and reward.

Crucially, neuroscience reveals that the highest spike of dopamine occurs during the anticipation of buying the item, not the actual ownership of it. The retail industry capitalizes on this chemical wave. The bright colors of a clearance sign, the smooth interface of a one-click checkout button, and the thrill of the hunt all trigger this reward loop, causing your logical prefrontal cortex to temporarily shut down.

The Emotional Triggers of Modern Retail Therapy

Most impulse buying is an unconscious attempt to regulate or alter your current emotional state. People rarely buy things impulsively when they are feeling completely balanced and grounded. Instead, sudden spending is typically triggered by:

-

Stress and Exhaustion: After a long, draining week at work, your willpower reserves are depleted. You buy something under the justification of, “I work hard; I deserve a treat.”

-

Boredom and Loneliness: Scrolling through online shopping apps provides an instant, easy distraction from a dull afternoon or a lonely evening.

-

Fear of Missing Out (FOMO): Flash sales, countdown timers, and “limited stock remaining” notifications create an artificial sense of scarcity, forcing you to buy out of panic rather than genuine need.

By recognizing that an impulse buy is often an emotional reaction rather than a logical decision, you can begin to build cognitive barriers between the initial desire and the final transaction.

Identify Your Personal Spending Triggers: The Crucial First Step to Awareness

You cannot fix a leak in your budget if you do not know where the water is coming from. To gain absolute control over your money, you must conduct an honest assessment of your personal spending habits to identify your specific retail vulnerabilities.

Digital vs. Physical Environmental Triggers

Different environments influence people in different ways. Some individuals are highly disciplined in physical brick-and-mortar stores but lose all control when browsing online marketplaces late at night. Others are the exact opposite, falling victim to strategically placed items in grocery store checkout lanes.

Take a moment to look back at your bank and credit card statements from the past three months. Highlight every purchase that wasn’t planned ahead of time. Ask yourself:

-

Where was I when I made this purchase?

-

What time of day was it?

-

What was my emotional state right before hitting buy?

The Dangerous Influence of Social Commerce

In the modern digital landscape, social media platforms have transformed into seamless, highly optimized shopping malls. Advanced algorithms track your browsing behavior, interests, and conversations to serve you hyper-targeted advertisements tailored directly to your subconscious desires. With integrated “Shop Now” buttons, the transition from viewing content to spending money takes less than five seconds.

If your financial leaks are consistently occurring via your smartphone, your digital environment is actively working against your long-term goals.

Deploy the 72-Hour Rule: The Ultimate Psychological Buffer for Smart Spending

The absolute gold standard for eliminating impulse purchases is creating a deliberate time buffer between the initial spark of desire and the actual transaction. The shorter the time window, the more likely you are to make an emotional, impulse-driven choice.

How to Implement the 72-Hour Rule

The rule is beautifully simple: Whenever you discover a non-essential item that you want to buy, you are forbidden from purchasing it immediately. Instead, you must write the item down on a dedicated piece of paper, a digital notes app, or a spreadsheet, along with the date and the price. Then, you must walk away and wait a full 72 hours (three days).

┌────────────────────────────────────────────────────────┐

│ THE 72-HOUR RULE PIPELINE │

├────────────────────────────────────────────────────────┤

│ 1. See an item you want impulsively. │

│ 2. DO NOT BUY. Add it to a "Waiting List" instead. │

│ 3. Wait exactly 72 hours. Let dopamine cool down. │

│ 4. Re-evaluate: Do I still need this item? │

│ ► YES: Buy it guilt-free if budgeted. │

│ ► NO: Delete from list. Money saved successfully! │

└────────────────────────────────────────────────────────┘

The Scientific Magic of the Cool-Down Window

During those three days, a fascinating psychological shift occurs. The initial dopamine rush fades completely, and your emotional attachment to the item drops significantly. Your logical brain regains control of your decision-making process.

When you review your waiting list after 72 hours, you will discover that in 70% to 80% of cases, you no longer care about the item, or you realize it is an unnecessary expense. For the remaining 20% that you still genuinely want, you can purchase them guilt-free, knowing the decision is rooted in value rather than an impulsive emotional whim.

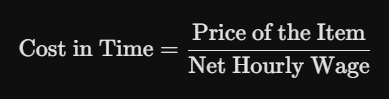

Calculate the True Cost of Items in Hours Worked: Shifting Your Perspective

Stop looking at price tags purely in terms of currency. When you view a shirt as costing $60, your brain easily rationalizes the transaction as a minor, manageable expense. To break the cycle of impulsive spending, you need to change the metric of cost from dollars to your personal life energy.

The Life Energy Equation

To apply this strategy, calculate your true net hourly wage. Take your monthly take-home pay (after taxes and deductions) and divide it by the total number of hours you work each month.

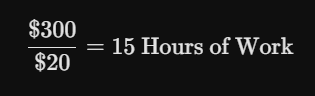

Example: If you bring home $3,200 a month after taxes and work a standard 160-hour month, your true net hourly wage is $20 per hour.

Translating the Price Tag

The next time you are tempted to impulsively buy an item online or in a store, take the retail price and divide it by your net hourly wage.

If you are looking at a sleek new electronic gadget or a luxury jacket that costs $300, perform the math:

Ask yourself an honest question: “Is this specific item worth sitting at my desk, enduring corporate stress, and trading away 15 hours of my finite life and energy?”

Framing purchases around your labor instantly changes your perspective on consumerism. It turns a trivial financial decision into a deep trade-off regarding your time, making it significantly easier to walk away from impulse buys.

Friction is Your Friend: How to De-Optimize Your Digital Shopping Experience

Retail tech companies spend millions of dollars minimizing friction in the purchasing pipeline. “Friction” refers to any step in the shopping process that forces a consumer to slow down, think, or exert effort. Features like saved credit card profiles, biometric facial recognition checkouts, and autofill shipping addresses are all designed to remove friction, ensuring you can spend money before your logical brain realizes what happened.

To protect your wallet, you must intentionally reintroduce friction into your digital ecosystem.

1. Delete Saved Credit Card Information

Go into your favorite online retailer accounts, digital wallets, and web browsers, and completely delete your saved credit card details.

When your card information is cleared, making an impulse purchase forces you to physically stand up, find your wallet, pull out the plastic card, and manually type in the 16-digit card number, expiration date, and CVV code. This minor physical hassle introduces a powerful pause button into your decision-making loop, giving you the time needed to reconsider the purchase.

2. Unsubscribe From Promotional Email Newsletters

Retail marketing emails are designed to manufacture artificial needs. They blast your inbox with subject lines like, “Flash Sale: 40% Off Ends Tonight!” or “Items are selling out in your cart!”

Spend 15 minutes utilizing a free cleanup tool or clicking the manual “Unsubscribe” button at the bottom of every retail marketing email you receive. If you don’t know a sale is happening, you won’t experience the artificial FOMO that drives emotional impulse buying.

3. Uninstall Retail Mobile Applications

If you carry a mobile shopping mall in your pocket 24/7, you are setting yourself up for financial failure. Uninstall shopping apps from your smartphone completely. If you truly need to buy something, force yourself to open a laptop, log into the web browser version, and navigate the platform manually. Increasing the structural effort required to browse drastically curtails mindless, late-night spending habits.

Master the “One-In, One-Out” Rule to Declutter Your Home and Budget

Impulse buying doesn’t just damage your bank account; it also creates physical clutter in your living space. Closets packed with unworn clothes, shelves lined with unread books, and drawers stuffed with unused gadgets are all physical manifestations of past impulse purchases.

To combat both financial drain and domestic clutter, implement a strict One-In, One-Out policy for your household.

┌────────────────────────────────────────┐

│ TEMPTED TO BUY A NEW LUXURY ITEM │

└────────────────────────────────────────┘

│

▼

┌────────────────────────────────────────┐

│ THE ONE-IN, ONE-OUT RULE │

├────────────────────────────────────────┤

│ To bring this NEW item home, you MUST │

│ donate, sell, or throw away an OLD, │

│ existing item within the same category.│

└────────────────────────────────────────┘

│

┌─────────────────────────────┴─────────────────────────────┐

▼ ▼

┌─────────────────────────────────┐ ┌─────────────────────────────────┐

│ I love my old item too much │ │ I am willing to sacrifice my old│

│ to throw it away or replace it.│ │ item for this upgrade. │

├─────────────────────────────────┤ ├─────────────────────────────────┤

│ ► DECISION: Cancel the buy. │ │ ► DECISION: Complete the buy │

│ Money stays in your pocket! │ │ guilt-free. Space stays even.│

└─────────────────────────────────┘ └─────────────────────────────────┘

How the Policy Works

Before you buy a new piece of clothing, kitchen appliance, pair of shoes, or home decor item, you must explicitly identify an existing item within that exact same category in your house that you are willing to sell, donate, or throw away the moment the new purchase arrives.

If you want to buy a new pair of sneakers, look at your closet. If you love your current shoe collection too much to part with any of them, you are legally barred from making the purchase. This rule forces you to evaluate whether the new item is genuinely superior to your current possessions, preventing duplicate spending and keeping your living space organized.

Switch to an All-Cash or Separate Allowance Architecture for Discretionary Spending

In our cashless, digital society, spending money has become entirely abstract. Tapping a plastic credit card, waving a smartwatch over a payment terminal, or clicking a digital button feels completely painless because you do not physically see or feel the wealth leaving your custody. This psychological detachment makes impulse buying incredibly easy.

To bring reality back to your finances, you need to change your transactional architecture.

The Cash Allowance Strategy

If you struggle with impulse purchases during weekend outings, grocery runs, or social gatherings, leave your credit cards at home in a locked drawer. Calculate a reasonable, fixed amount of discretionary “fun money” for the week, withdraw that exact amount in physical paper bills from an ATM, and place it in your wallet.

When you shop with physical cash, you experience real, psychological friction. As you physically hand over paper bills to a cashier, you watch your cash supply visibly shrink. Once the physical cash in your wallet hits zero, your spending for that week is over.

The Dual Checking Account System

If you prefer a digital lifestyle, set up a Dual Checking Account system at your bank to isolate your funds:

-

Account A (The Bills Hub): This account receives your monthly paycheck. All your mandatory fixed expenses (rent, utilities, insurance, loan minimums) are paid automatically out of this hub. Your credit cards are tied exclusively to this account only for pre-planned necessities.

-

Account B (The Allowance Hub): Every month, you transfer a strict, predetermined budget for discretionary spending into this second account, which is tied to a standard debit card.

When you go out with friends or browse online, you use only the Account B debit card. If you see an attractive item but the balance in Account B is running low, you cannot purchase it. This setup protects your critical bill money from accidental, impulsive spending sprees.

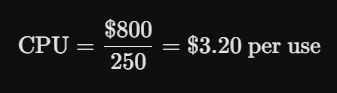

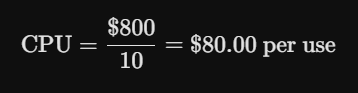

Adopt the “Cost-Per-Use” Mindset for High-Value Purchases

Not all impulse purchases are small, low-cost items. Occasionally, individuals make sudden, large-scale financial commitments, such as high-end fitness equipment, advanced kitchen appliances, or expensive hobby gear, under the rationalization that the item will change their lifestyle for the better.

To determine whether a high-cost purchase is financially justifiable, shift your thinking from the total retail price to your expected Cost-Per-Use (CPU).

Evaluating a Large Expenditure

Imagine you are walking through an electronics store and feel a sudden urge to buy an advanced espresso machine that costs $800. Your impulse-driven brain rationalizes: “This will save me money on coffee shop trips!”

Before checking out, run a realistic CPU projection for the next year:

-

Scenario A (Realistic Daily Habit): You use the machine 250 times over the coming year.

Over time, this item matches your lifestyle and could eventually save you money compared to high-end coffee shop prices.

-

Scenario B (The Reality of Impulse Buys): You use the complex machine enthusiastically for the first two weeks, get tired of the cleaning routine, and relegate it to the back of the pantry. You use it a total of 10 times over the course of the year.

Before making any major, high-cost purchase, look back at your history. If you have a habit of abandoning new hobbies after a few weeks, save your money. Rent the equipment first, borrow it from a friend, or buy a cheap secondhand version to prove the habit is real before committing significant capital to a top-tier model.

Build an Intentional “Wish List” Spreadsheet to Channel Shopping Desires

Eliminating impulse buying does not mean you can never buy nice things for yourself again. The goal of personal finance is to ensure your money is channeled toward things that bring true, lasting value to your life. A highly effective tool to manage your desires is maintaining an automated, centralized Wish List Spreadsheet.

Constructing Your Wish List Architecture

Create a simple spreadsheet using a cloud drive with four specific columns:

-

Item Name & Description

-

Retail Price & Direct Web Link

-

The Date Added to the Spreadsheet

-

The Core Value Justification (Why do I need this?)

Whenever you discover something you want to buy, you are not allowed to purchase it on the spot. Instead, you add it to your Wish List Spreadsheet.

Leveraging Your Birthday and Holiday Celebrations

Keep this spreadsheet active year-round. When a holiday, birthday, or milestone celebration approaches and family members ask what gifts you would enjoy, share the link to your wish list.

This channels your past shopping impulses into a structured repository for meaningful gifts, saving your family members from guessing what to buy while completely protecting your own personal bank accounts from lifestyle drain.

Turn Financial Milestones Into Games to Make Saving Money Fun

One reason people fall victim to impulse buying is that shopping provides an instant hit of excitement, whereas saving money in a standard bank account can feel boring, abstract, and slow. To combat this psychological imbalance, gamify your personal finances to make saving money just as rewarding as spending it.

1. The “Zero Spend” Monthly Challenge

Pick one month out of the calendar year to execute a strict “Zero Spend” or “No-Buy” challenge. During these 30 days, you lock down your finances completely. You are legally allowed to spend money only on absolute survival essentials: rent, basic groceries, utilities, and mandatory medicines.

All discretionary spending—dining out, apparel, entertainment, and digital subscriptions—is paused. Track your consecutive “clean days” on a physical wall calendar using a bright marker. Gamifying your discipline this way resets your baseline spending habits and highlights how little consumer goods you actually need to be happy.

2. The “Match Your Impulse” Savings Penalty

If you find yourself on the verge of breaking your rules and making an impulse buy, institute an internal financial tax. For every dollar you spend on an unplanned luxury item, you must instantly transfer an equivalent dollar amount out of your checking account and into a long-term investment or retirement account.

If you want to buy an unplanned $100 pair of designer sunglasses, the rule states you must also find an extra $100 to deposit straight into your investment portfolio. If you cannot afford the $100 investment match, you cannot afford the sunglasses. This internal rule doubles the immediate financial cost of your bad habits, creating the structural friction needed to change your behavior.

Establish an Accountability Partnership to Maintain Long-Term Discipline

Human beings are inherently social creatures. We find it significantly easier to maintain discipline and build healthy long-term habits when we are working in coordination with an supportive community rather than fighting temptation in absolute isolation.

The Role of an Accountability Partner

Find a trusted friend, family member, or spouse who shares your values and goals regarding financial responsibility. Sit down with them and establish an explicit Accountability Agreement.

-

Share Your Financial Goals: Tell them exactly what you are saving for (e.g., clearing your student loans, accumulating a down payment for a house, or building a 6-month safety net).

-

The Check-In Routine: Establish a rule where you must text or call your partner before making any unplanned purchase over a specific dollar threshold (such as $50 or $100).

-

Review Progress Together: Schedule a brief monthly coffee date or phone call to review your bank statement wins and reflect on any moments where you stumbled.

Knowing that you have to explain an impulsive, emotional purchase to a respected partner introduces a powerful layer of social accountability that easily overpowers the fleeting temptation of an online sale banner.

What to Execute Today to Clear Out Impulse Spending

Transforming your relationship with money does not require overnight perfection. It requires building reliable systems that protect you from your own emotional moments. Take control of your finances right now by executing these three immediate tasks:

-

Action 1: Delete Your Cards. Open your smartphone and internet browsers right now, navigate to your saved payment settings, and delete your credit card numbers from your auto-fill profiles.

-

Action 2: Create Your Waiting List. Open a new page in your notes app or grab a physical notebook and label it “My 72-Hour Waiting List.” Commit to routing all future unplanned desires through this list.

-

Action 3: Clean Your Inbox. Spend the next 10 minutes opening the promotional retail emails sitting in your inbox, scrolling to the bottom, and hitting the unsubscribe links. Clean out the marketing noise.

Impulse buying is a design trap engineered by modern retailers, but you have the psychological tools and tactical habits to defeat it. By introducing friction into your digital lifestyle, tracking costs in hours worked, and utilizing structural time buffers, you can eliminate buyer’s remorse, secure your cash flow, and build a stable financial future filled with true freedom and peace of mind.