Learn how to create a financial plan for the coming years

Imagine driving down an unfamiliar highway in the middle of a heavy storm without a GPS or a dashboard. You don’t know how much fuel you have left, how fast you are moving, or exactly where the next exit is. For most people, this is exactly how they manage their financial lives. They move forward blindly, hoping they will randomly arrive at a secure, comfortable retirement.

Hoping for financial security is not a strategy. True wealth, stability, and freedom are built through intentional design. A long-term financial plan is the GPS for your money. It maps out your current financial position, highlights potential road hazards, and calculates the exact turns you need to take to reach your ultimate destination over the next few years.

Whether you want to buy a home, start a business, fund your children’s education, or achieve absolute financial independence, you need a structured framework to get there. This comprehensive guide breaks down exactly how to construct a robust, comprehensive financial plan from scratch, ensuring your money works for your future self.

What is a Long-Term Financial Plan and Why Do You Need One Right Now?

Before diving into the spreadsheets and numbers, it is vital to understand what a financial plan actually is. Many people mistake budgeting for financial planning. While budgeting tracks your monthly cash inflow and outflow, a financial plan is much broader. It looks years or even decades into the future, aligning your daily spending habits with your deepest life goals.

The True Value of Forward-Looking Financial Design

A well-constructed multi-year financial plan offers three primary benefits:

-

Elimination of Financial Anxiety: When you have a plan, unexpected market fluctuations or personal emergencies cease to be catastrophic events. They become variables you have already accounted for.

-

Hyper-Intentional Spending: A plan gives every dollar you earn a clear purpose. It eliminates the guilt often associated with discretionary spending because you know your future milestones are already funded.

-

The Power of Compounding Momentum: Small, consistent financial adjustments made today multiply exponentially over a multi-year timeline, turning modest savings into substantial wealth.

Without a forward-looking plan, you are vulnerable to lifestyle creep—the tendency to increase your spending at the exact same rate as your income grows, leaving you perpetually trapped on a financial hamster wheel.

Conducting a Deep-Dive Financial Audit: Establishing Your Current Baseline

You cannot plan a route to a future destination if you do not know your exact starting coordinates. The first structural step of multi-year planning is conducting an incredibly honest, comprehensive financial audit of your current assets, liabilities, and habits.

1. The Net Worth Calculation

Your net worth is the absolute truth metric of your financial life. It strips away the illusion of high income or luxury possessions and reveals your true financial baseline. To calculate it, use this formula:

-

Liquid Assets: Cash in checking accounts, high-yield savings accounts (HYSAs), and short-term certificates of deposit (CDs).

-

Investment Assets: Retirement accounts (401k, Roth IRA, Traditional IRA), brokerage accounts, mutual funds, and cryptocurrency.

-

Physical Assets: The realistic market value of your primary residence, real estate holdings, and vehicles.

-

Liabilities: The total remaining balances on your mortgage, student loans, auto loans, credit cards, and any outstanding personal debt.

Write this final number down. If it is negative, do not despair. This is simply your starting line. Your entire multi-year plan will be engineered to drive this number steadily upward.

2. The Structural Cash Flow Analysis

Next, look backward at your last three to six months of bank and credit card statements. Calculate your exact Net Monthly Cash Flow:

Categorize your spending into Fixed Commitments (housing, utilities, insurance, minimum debt payments) and Variable Lifestyle Expenditures (dining out, travel, entertainment, subscriptions). The money left over after subtracting these categories is your financial surplus—the raw capital you will use to fund your multi-year goals.

Setting SMART Financial Goals Across Multiple Timelines

A financial plan without explicit goals is simply math for the sake of math. To drive long-term discipline, you must convert your vague dreams (“I want to be rich,” “I want to buy a house”) into highly specific financial milestones organized by priority and timeline.

To make your goals effective, pass them through the SMART framework: Specific, Measurable, Achievable, Relevant, and Time-bound.

| Goal Timeline | Horizon | Core Focus Area | Practical Example |

| Short-Term | 0 – 12 Months | Stabilization & Safety | Save a full $5,000 emergency fund in a High-Yield Savings Account. |

| Mid-Term | 1 – 5 Years | Growth & Lifestyle Milestones | Amass a $40,000 cash down payment for a primary home purchase. |

| Long-Term | 5+ Years | Absolute Independence | Scale investment portfolios to achieve a $1.2 million retirement nest egg. |

The Power of Granular Micro-Milestones

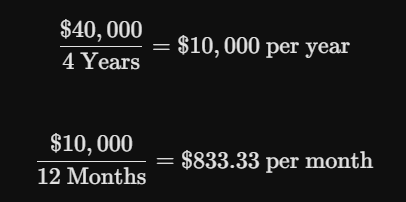

Large goals like saving $40,000 for a house down payment in four years can feel completely overwhelming. To maintain motivation, break the macro-goal down into digestible micro-milestones.

Now, your goal is no longer finding a massive lump sum of $40,000; your goal is adjusting your monthly budget to free up exactly $833.33 per month. This shifts your psychological focus from an unreachable distant future to an actionable, daily habit.

Optimizing Your Savings Architecture: The Emergency Fund Evolution

The foundation of any multi-year financial plan is a robust risk management system. If you begin investing or paying off long-term debt without securing your base layout, a single corporate layoff, medical emergency, or economic downturn can wipe out years of progress.

Transitioning From a Starter Fund to a Strategic Reserve

If you are starting from scratch, your immediate short-term priority is a $1,000 to $2,000 starter emergency fund. This keeps you from backsliding into high-interest credit card debt when minor issues arise.

However, a true multi-year plan requires a Strategic Emergency Reserve equivalent to 3 to 6 months of your absolute baseline living expenses.

-

When to target 3 months: You work in a high-demand industry with extreme job security, have multiple independent streams of household income, and possess no dependents.

-

When to target 6 months (or more): You are a freelancer, business owner, single-income earner, or work in a highly volatile, cyclical sector.

Maximizing Cash Efficiency via High-Yield Savings Accounts

Never let your strategic emergency reserve sit in a traditional checking or savings account earning a negligible 0.01% interest rate. Over a multi-year timeline, inflation will silently erode the purchasing power of that cash.

Instead, house your emergency reserves in a separate, insured High-Yield Savings Account (HYSA). HYSAs offer significantly higher interest rates while maintaining absolute liquidity, meaning your money stays completely safe and accessible while actively growing to outpace inflationary pressures.

Constructing a Multi-Year Debt Elimination Strategy

High-interest consumer debt is the single greatest destroyer of wealth building potential. It acts as a structural leak in your financial plan, transferring your earnings to major lenders via compounding interest. To fund your future years, you must plug this leak permanently.

When designing a multi-year debt payoff plan, choose between two primary operational frameworks:

The Debt Avalanche Framework (The Mathematical Mastermove)

The Avalanche method focuses entirely on minimizing your total cost of credit.

-

List all outstanding debts in order from the highest annual percentage rate (APR) to the lowest.

-

Maintain the bare minimum payments on all accounts except the one with the highest APR.

-

Direct every available dollar of your financial surplus into that highest APR debt.

-

Once eliminated, roll that entire payment capacity into the next highest APR debt.

Why it works: This is the most efficient mathematical strategy. It minimizes the total interest you pay over the coming years and clears your debt path as quickly as possible.

The Debt Snowball Framework (The Psychological Momentum Builder)

The Snowball method prioritizes human psychology and emotional validation.

-

List all outstanding debts in order from the smallest total balance to the largest balance, regardless of the interest rates.

-

Pay minimums on everything except the smallest balance.

-

Throw your extra surplus funds at the smallest balance until it hits zero.

-

Roll that victory momentum and cash capacity into the next smallest balance.

Why it works: For many individuals, seeing entire accounts close quickly builds immense psychological momentum, providing the emotional stamina required to stay disciplined over a multi-year timeline.

Designing a Multi-Year Investment Strategy for Generational Wealth

Once your emergency reserves are funded and your high-interest debt is eliminated, your financial surplus changes roles. It transforms from a defensive shield into an offensive weapon designed to build long-term wealth through investing.

1. Harnessing the Tax Advantages of Retirement Accounts

The easiest way to optimize your investment strategy over the next few years is to utilize tax-advantaged accounts provided by your employer or the government.

-

Employer-Sponsored Plans (e.g., 401k): If your employer offers a matching contribution program (e.g., matching up to 4% of your salary), this is literally free money. Your absolute baseline investment goal should be contributing enough to capture the maximum employer match.

-

Individual Retirement Accounts (IRAs): Explore both Traditional and Roth IRAs. A Roth IRA allows you to invest after-tax dollars today, meaning your investments grow completely tax-free, and your withdrawals during retirement are 100% tax-exempt. This is an incredibly powerful vehicle for multi-year compounding growth.

2. The Core-and-Satellite Investment Philosophy

For your taxable brokerage accounts, avoid the trap of day trading, timing the market, or chasing speculative individual stocks. Instead, adopt a passive, long-term approach based on low-cost Index Funds or Exchange-Traded Funds (ETFs) that track broad market indices like the S&P 500 or the total global stock market.

By automating your investments through Dollar-Cost Averaging (DCA)—investing a fixed amount of money every single month regardless of whether the market is up or down—you remove emotion from the equation and buy more shares when prices are low, locking in immense multi-year upside.

Protecting Your Blueprint: The Critical Role of Insurance and Risk Management

A brilliant financial plan can be completely derailed in a single afternoon if you fail to protect your assets. True financial planning requires defensive engineering in the form of proper insurance coverage.

As you plan out the coming years, ensure your risk management portfolio includes these non-negotiable coverages:

1. Health and Disability Insurance

Medical crises are the leading cause of personal bankruptcy. Ensure you maintain comprehensive health insurance. Furthermore, consider Long-Term Disability Insurance, which protects your single greatest financial asset: your ability to earn an income. If an illness or injury prevents you from working for an extended period, disability insurance replaces a massive percentage of your salary, keeping your financial plan alive.

2. Term Life Insurance

If you have anyone in your life who depends on your income—such as a spouse, children, or aging parents—Term Life Insurance is mandatory. Avoid complex, high-fee permanent or whole-life products unless you have highly specific estate planning needs. Stick to low-cost term life insurance that covers the exact span of years until your dependents are self-sufficient or your investment portfolio reaches maturity.

Tax Optimization: Strategies to Legally Minimize Your Annual Tax Burden

Tax planning is not a task you do once a year in April. It is a continuous, year-round component of a successful multi-year financial strategy. The less money you legally pay in taxes, the more capital you retain to compound over the coming years.

Strategic Tax-Loss Harvesting

In your taxable brokerage accounts, you can utilize Tax-Loss Harvesting to offset your tax liabilities. This involves strategically selling specific investments that have experienced a decline in value. By realizing those losses, you can offset your capital gains from other investments or write off up to $3,000 of ordinary income each year, keeping more cash in your wealth-building ecosystem.

Maximizing Deductions and Pre-Tax Vehicles

Look for ways to lower your Adjusted Gross Income (AGI). Contributing to pre-tax accounts like a traditional 401k or a Health Savings Account (HSA) instantly lowers your taxable income for the year. An HSA is particularly powerful because it features a triple tax advantage: contributions are tax-deductible, funds grow tax-free, and withdrawals are entirely tax-free if used for qualified medical expenses.

Automating Your Financial Ecosystem: Removing Human Willpower

The secret to executing a financial plan over a multi-year horizon is removing human error, emotion, and decision fatigue. If you have to manually calculate your savings, transfer your investment funds, and pay your bills every single month, your plan will eventually fail during a stressful month.

By building a self-managing automated infrastructure, your money naturally flows into its designated strategic channels the moment your paycheck hits your account.

┌────────────────────────────────────────┐

│ MONTHLY INCOME SOURCE │

└────────────────────────────────────────┘

│

┌─────────────────────────────┼─────────────────────────────┐

▼ ▼ ▼

┌─────────────────┐ ┌─────────────────┐ ┌─────────────────┐

│ Fixed Expenses │ │ Strategic HYSA │ │ Investment Hub │

├─────────────────┤ ├─────────────────┤ ├─────────────────┤

│ Automated Bill │ │ Automated App │ │ Automated DCA │

│ Pay (Housing, │ │ Transfer │ │ Into Broad │

│ Utilities, etc.)│ │ (Emergency/Goals│ │ Index Funds/IRAs│

└─────────────────┘ └─────────────────┘ └─────────────────┘

Set up automatic transfers so that your short-term savings, retirement allocations, and investment contributions are processed immediately on payday. When you “pay yourself first” via automation, you force yourself to comfortably build your lifestyle around the remaining checking balance, guaranteeing consistent progress toward your multi-year milestones.

Reviewing and Calibrating Your Financial Plan: The Annual Audit Routine

A financial plan is not a static document that you write once and lock away in a drawer forever. It is a living, dynamic blueprint that must shift and evolve as your life changes. Over the next few years, you will experience career changes, income fluctuations, family updates, and shifting personal priorities.

The Bi-Annual and Annual Adjustment Habit

Schedule a recurring date with yourself (and your partner, if applicable) every six to twelve months to review your plan. During this calibration session, analyze the following factors:

-

Asset Allocation Rebalancing: Have market movements caused your investment portfolio to become too risky or too conservative? Adjust your holdings back to your target asset allocation.

-

Income Increases (Lifestyle Inflation Control): If you received a raise or a bonus, did you automatically increase your discretionary spending, or did you direct that new capital toward accelerating your long-term goals?

-

Major Life Transitions: Did you get married, welcome a new child, change careers, or relocate? Update your short-term and mid-term goal tracking to reflect these changes.

An effective plan does not require perfection; it requires consistent, intentional course corrections over time to keep you aligned with your true north.

Step-by-Step Action Plan: What to Do Today to Start Your Multi-Year Plan

Building a comprehensive financial plan can feel like a massive undertaking, but you can break through any paralysis by taking a few immediate, simple actions right now:

-

Calculate Your Baseline Net Worth Today: Open your accounts, pull up a spreadsheet or a piece of paper, and list your total assets minus your liabilities. Face your true starting point.

-

Establish One Clear SMART Mid-Term Goal: Pick one milestone you desperately want to achieve within the next three years (e.g., clearing a specific loan or building an investment floor) and calculate the exact monthly savings required to hit it.

-

Automate Your First Micro-Transfer: Log into your primary banking portal and establish an automatic recurring transfer of any manageable amount (even if it is just $50 a month) straight into a separate High-Yield Savings Account.

By shifting your focus from daily survival to a structured multi-year strategy, you transform your relationship with money. You cease to be a passive observer of your financial life and become the active designer of your financial freedom. Use this guide as your operational blueprint, stay disciplined through automation, and watch your wealth grow systematically over the coming years.