What Is a Trading Commission?

In the modern financial landscape of 2026, the term “trading commission” might seem like a relic of the past. If you open a mobile brokerage app today, you’re likely greeted with bold banners promising “$0 Commission Trades.” To a beginner, this sounds like the ultimate win—a gateway to Wall Street with no cover charge.

However, in the world of finance, the old adage remains true: if you aren’t paying for the product, you are the product.

Understanding what a trading commission is, how it has evolved, and the “invisible” costs that have replaced it is essential for anyone looking to build a serious investment portfolio. This guide will walk you through everything you need to know about trading commissions, brokerage fees, and how to keep more of your money working for you.

Understanding Trading Commissions: A Beginner’s Definition

At its simplest level, a trading commission is a service fee charged by a broker to execute a trade on your behalf. Think of it as a “delivery fee” for your stocks. When you want to buy 10 shares of a company, you don’t go to the company’s headquarters; you go to a broker who has access to the stock exchange. The commission is the price you pay the broker for providing that access and handling the paperwork.

The Mechanics of the Fee

Historically, commissions were charged in two primary ways:

-

Flat Fee: You pay a set amount (e.g., $6.95) regardless of how many shares you buy.

-

Percentage-Based: The broker takes a small cut (e.g., 0.1%) of the total dollar value of the trade.

In the past, these fees were a significant barrier to entry. If you only had $100 to invest and the commission was $10, you were immediately down 10% on your investment before the stock even moved a penny.

The Evolution of Brokerage Fees: From Fixed Rates to “Free” Trading

To understand where we are in 2026, we have to look back at the “May Day” of 1975. Before this date, the New York Stock Exchange (NYSE) required all brokers to charge the same fixed commission rates. When these rules were abolished, it gave birth to the discount broker.

The Robinhood Effect

The real seismic shift occurred in the mid-2010s when platforms like Robinhood introduced commission-free trading. To stay competitive, legacy giants like Fidelity, Charles Schwab, and E*TRADE were forced to drop their commissions to zero for US stocks and ETFs.

While this democratized investing, it changed the brokerage business model forever. Brokers still have employees to pay and servers to maintain. If they aren’t charging you $6.95 per trade, they are making money elsewhere—often in ways that are less transparent to the average investor.

How Brokerages Make Money if Commissions Are Zero?

This is the most important section for any beginner to understand. “Zero commission” does not mean “zero cost.” When a brokerage removes the upfront commission, they typically pivot to one of the following revenue streams:

1. Payment for Order Flow (PFOF)

This is the most controversial replacement for commissions. Instead of sending your “Buy” order directly to the New York Stock Exchange, your broker sends it to a “Market Maker” (a massive high-frequency trading firm). The Market Maker pays your broker a small fee for the right to execute your trade.

The risk for the investor is that the Market Maker might not give you the absolute best price available on the public market. You might save $5 on a commission but lose $6 because you bought the stock at a slightly higher price than necessary.

2. The Bid-Ask Spread

The spread is the difference between the highest price a buyer is willing to pay (the bid) and the lowest price a seller is willing to accept (the ask).

-

Bid: $150.00

-

Ask: $150.05

-

Spread: $0.05

When you place a “Market Order,” you usually buy at the Ask and sell at the Bid. That $0.05 difference is a “hidden” commission that goes to the market participants facilitating the trade.

3. Net Interest Margin

Brokerages make a massive amount of money on the “uninvested cash” sitting in your account. If you have $1,000 in your brokerage account that isn’t currently in stocks, the broker might move that money into a bank account that earns 5% interest, while only giving you 0.01% interest. They pocket the difference.

Commissions vs. Fees: Defining the Distinctions

In your monthly statement, you will see a variety of charges. It is important to distinguish between a commission and a regulatory fee.

-

Trading Commission: A discretionary fee charged by the broker for their service.

-

SEC Section 31 Fee: A government fee charged by the Securities and Exchange Commission to cover the costs of regulating the equities markets. In 2026, this is usually a few cents per $10,000 of sales.

-

FINRA TAF (Trading Activity Fee): A small fee charged by the Financial Industry Regulatory Authority to recover the costs of supervision and regulation.

While commissions are often zero, these regulatory fees are mandatory and will always appear when you sell a security.

Asset-Specific Commissions: Why Some Trades Still Cost Money

While most US-based stocks and ETFs are now commission-free, other asset classes still carry costs.

1. Options Commissions

Trading options usually involves a “per contract” fee. While the base commission might be $0, you will often pay $0.50 to $0.65 per contract.

If you buy 10 contracts, you are paying $6.50. This is to cover the higher complexity and risk management associated with derivatives.

2. Cryptocurrency Commissions

Crypto is the “Wild West” of commissions. Some platforms charge a flat percentage (e.g., 1.49%), while others bake the commission into a massive spread. It is common for a beginner to buy $100 of Bitcoin and immediately see their balance reflect $97 due to high entry fees.

3. Mutual Fund Transaction Fees

While most brokers offer a list of “No-Transaction-Fee” (NTF) mutual funds, buying a fund that is not on that list can be incredibly expensive—sometimes costing $20 to $50 per trade.

The Long-Term Impact of Commissions on Your Wealth

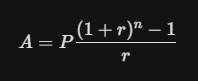

For a long-term investor, even a small commission can act as a “reverse compound interest” drag on your portfolio. Let’s look at the math.

Imagine you invest $500 every month into a portfolio that earns an 8% annual return.

Scenario A: Zero Commissions

Your full $500 goes to work every month. After 30 years, using the standard compound interest formula:

Your total would be approximately $745,000.

Scenario B: $10 Commission per Trade

Only $490 goes to work. After 30 years, your total would be approximately $730,000.

Those “small” $10 fees cost you $15,000 in future wealth. This is why the move to zero-commission trading has been such a massive boon for the average retail investor in the United States.

How to Minimize Trading Commissions and Fees in 2026

Even in a “free” world, there are ways to optimize your costs. Here are three expert strategies for beginners:

1. Use Limit Orders Instead of Market Orders

A Market Order tells the broker, “Buy this right now at whatever the price is.” This leaves you vulnerable to wide spreads.

A Limit Order tells the broker, “Only buy this if the price is $X or lower.” This gives you control over the execution price and helps mitigate the “hidden” cost of the spread.

2. Consolidate Your Trades

If you are trading an asset that still carries a flat fee (like certain international stocks or mutual funds), avoid making small, frequent purchases. Instead of buying $100 ten times (paying the fee ten times), wait until you have $1,000 and make one single purchase.

3. Watch the “Expense Ratio”

In the world of ETFs, the commission is what you pay to enter the store, but the Expense Ratio is what you pay to stay in the store. This is a management fee taken directly from the fund’s assets. A “free” commission on an ETF with a 1% expense ratio is a bad deal compared to a $5 commission on an ETF with a 0.03% expense ratio.

The Future of Trading: Commissions in the Age of AI

As we progress through 2026, we are seeing the rise of AI-Optimized Execution. New brokerage features are using artificial intelligence to “hunt” for the best possible price across dozens of exchanges, effectively bypassing the downsides of Payment for Order Flow.

We are also seeing the expansion of Subscription-Based Brokerage. Instead of commissions, some firms are charging a flat monthly fee (e.g., $10/month) for a “Pro” suite that includes zero-commission options, higher interest on cash, and better research tools. For active traders, this is often cheaper than paying per-contract fees.

Don’t Let the “Free” Label Blind You

A trading commission is just one piece of the financial puzzle. While the headline price of $0 is a wonderful development for the democratization of finance, a smart investor looks deeper.

When choosing a brokerage, ask yourself:

-

How good is their order execution?

-

What is the interest rate they pay on my idle cash?

-

Are there hidden fees for moving my money out (ACATS fees)?

In 2026, the best “commission” is the one you understand. By knowing the difference between upfront costs, spreads, and PFOF, you can navigate the markets with the confidence of a professional and ensure that your hard-earned money is building your future, not your broker’s.