Tips for achieving financial independence

Financial independence is often mistaken for being “rich” or having a garage full of luxury cars. However, in the world of modern finance, the definition is far more empowering: it is the point where your passive income—money earned from investments, businesses, or assets—covers all your living expenses. It means work becomes a choice, not a necessity.

Achieving this milestone isn’t reserved for lottery winners or Wall Street executives. It is a marathon that requires a blend of discipline, strategic planning, and a deep understanding of how money works. Whether you are just starting your career or looking to pivot your financial future, this comprehensive guide will walk you through the essential steps to reclaiming your time and building lasting wealth.

1. Defining Your “Why”: The Psychology Behind Financial Freedom

Before looking at spreadsheets or stock charts, you must understand your motivation. Financial independence (FI) is 20% head knowledge and 80% behavior. Without a strong “why,” the sacrifices required to save and invest will feel like a burden rather than a bridge to a better life.

For some, the “why” is the ability to travel the world. For others, it’s the peace of mind that comes from knowing their family is secure regardless of the economic climate. When you define your purpose, you stop viewing “saving” as a restriction and start viewing it as “buying your freedom.”

2. Tracking Your Net Worth and Cash Flow for Maximum Visibility

You cannot manage what you do not measure. To reach financial independence, you need a clear picture of two specific metrics: your Net Worth and your Cash Flow.

-

Net Worth: This is the “big picture.” Calculate it by subtracting all your liabilities (debts) from your assets (savings, investments, home equity). Tracking this monthly allows you to see the tangible progress of your wealth-building journey.

-

Cash Flow: This is the day-to-day movement of money. Where is every dollar going? Use a tracking app or a simple spreadsheet to categorize your spending. You might be surprised to find that “leaks” in your budget—like unused subscriptions or frequent dining out—are draining thousands of dollars per year that could be working for you in the market.

3. High-Impact Budgeting Strategies: The “Pay Yourself First” Method

Traditional budgeting often fails because it feels like a diet. Instead of trying to restrict every penny, use the “Pay Yourself First” model.

As soon as your paycheck hits your account, automatically move a predetermined percentage (ideally 20% or more) into your investment or savings accounts. By automating this process, you treat your future self as your most important “bill.” You then live off whatever is left. This removes the willpower struggle and ensures that your path to independence is consistent and non-negotiable.

4. Eliminating Toxic Debt: The Anchor Holding You Back

Not all debt is created equal, but high-interest consumer debt—specifically credit cards—is the greatest enemy of financial independence. If you are paying 20% interest on a credit card while the stock market is returning 8–10%, you are effectively losing money every month.

Consider two popular strategies for debt elimination:

-

The Debt Snowball: Pay off your smallest debts first to build psychological momentum.

-

The Debt Avalanche: Pay off debts with the highest interest rates first to save the most money in the long run.

Whichever method you choose, the goal is the same: stop paying interest to others so you can start earning interest for yourself.

5. Building an Antifragile Emergency Fund

Life is unpredictable. A medical emergency, a sudden job loss, or a major home repair can derail a financial plan if you aren’t prepared. Before you dive deep into aggressive investing, you need a “safety net.”

A standard emergency fund consists of three to six months of living expenses held in a high-yield savings account. This isn’t an investment meant to make you rich; it is insurance for your lifestyle. Having this cash cushion prevents you from having to sell your investments during a market downturn, which is one of the most common ways people lose wealth.

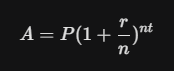

6. The Magic of Compounding: Why Time is Your Greatest Asset

The most powerful force in finance is compound interest. Albert Einstein famously called it the “eighth wonder of the world.” Compounding happens when the earnings on your investments begin to earn their own earnings.

In simple terms: if you invest $500 a month starting at age 25, you will likely have significantly more wealth by age 65 than someone who invests $1,500 a month starting at age 45. The lesson is clear: don’t wait for the “perfect” time or a higher salary. Start with whatever you have today to give your money more time to grow.

7. Strategic Asset Allocation: Building a Diversified Investment Portfolio

To achieve financial independence, your money needs to work harder than you do. This requires moving beyond a simple savings account and into the world of investing.

For the average person, Low-Cost Index Funds are often the most effective tool. These funds allow you to own a small piece of hundreds or thousands of companies simultaneously. This diversification protects you from the failure of a single company while allowing you to capture the overall growth of the economy.

Key assets to consider for a balanced portfolio include:

-

Equities (Stocks): For long-term growth.

-

Fixed Income (Bonds): For stability and income.

-

Real Estate: For tangible assets and potential rental income.

-

Cash Equivalents: For liquidity and short-term needs.

8. Tax Optimization: How to Legally Keep More of Your Earnings

It’s not about how much you make; it’s about how much you keep. Understanding the tax code is a “pro-level” strategy for reaching financial independence faster. In the United States and many other developed nations, governments provide tax-advantaged accounts to encourage saving for the future.

Utilizing accounts like a 401(k), IRA, or HSA can significantly reduce your tax burden. Some accounts allow you to invest “pre-tax” dollars (lowering your current taxable income), while others, like the Roth IRA, allow your money to grow and be withdrawn completely tax-free. Over a 30-year career, tax optimization can result in hundreds of thousands of dollars in additional wealth.

9. Defeating Lifestyle Inflation: The Silent Wealth Killer

As people earn more, they tend to spend more. This is known as Lifestyle Inflation. You get a 10% raise, so you buy a car with a 10% higher payment. You get a bonus, so you upgrade to a bigger apartment.

If your expenses rise at the same rate as your income, you will never reach financial independence, regardless of how much you earn. The secret to fast-tracking your freedom is to keep your expenses relatively stable as your income grows. This widens the “gap”—the surplus money available for investing—which is the true engine of wealth.

10. Generating Multiple Streams of Income and Side Hustles

Relying on a single source of income is a risk. Most people who achieve financial independence early do so by diversifying their income. This doesn’t mean you need three jobs; it means you should look for ways to decouple your time from your earnings.

-

Dividend Investing: Buying stocks that pay you a portion of their profits regularly.

-

Real Estate: Earning monthly rent from properties.

-

Digital Products: Creating an e-book or course that sells while you sleep.

-

Small Business Ownership: Building a systemized business that doesn’t require your daily presence.

11. The 4% Rule: Calculating Your Financial Independence Number

How do you know when you’ve actually “made it”? Financial experts often point to the 4% Rule. This rule suggests that if you can live off 4% of your total investment portfolio annually, your money has a very high probability of lasting 30 years or more.

To find your “FI Number,” multiply your annual expenses by 25. For example, if you need $40,000 a year to live comfortably, your target is $1,000,000 ($40,000 x 25). Once you hit that number, you are mathematically independent.

12. Maintaining Physical and Mental Health as an Investment

There is no point in reaching financial independence if you are too unwell to enjoy it. Health is the ultimate form of wealth. High medical costs are one of the leading causes of bankruptcy, and chronic stress from overworking can lead to long-term health complications.

Investing in a good diet, regular exercise, and mental health care isn’t just a lifestyle choice—it’s a financial strategy. A healthy body reduces long-term expenses and gives you the energy needed to pursue your goals with intensity.

Your Journey Starts with a Single Step

Reaching financial independence is not an overnight event; it is a series of small, intentional choices made over many years. It requires saying “no” to temporary pleasures so you can say “yes” to permanent freedom.

Start by tracking your spending this week. Identify one unnecessary expense and redirect that money into an investment account. Over time, these small shifts will snowball into a mountain of wealth that provides you with the most valuable commodity on earth: the ability to spend your time exactly how you choose.