The Hidden Cost of Bad Financial Habits

We like to think of our financial lives as a series of big, momentous decisions: buying a home, choosing a career path, or investing in a bull market. While those moments matter, the reality of your wealth—or the lack thereof—is actually determined by the quiet, invisible habits you perform every single day.

Bad financial habits are like a slow leak in a massive ship. You might not notice the water at first, but over time, the weight drags you down until the vessel is no longer seaworthy. The most dangerous thing about these habits is their hidden cost. It isn’t just the $5 you spent on a coffee; it is the thousands of dollars that $5 could have become if it had been put to work.

In this deep dive, we will peel back the curtain on the silent wealth-killers and explore the true cost of the habits your bank account wishes you’d break.

The Opportunity Cost: The Ghost of Future Wealth

In the world of finance, every dollar has two values: its face value today and its potential value in thirty years. When you develop a bad spending habit, you aren’t just losing the cash in your wallet; you are sacrificing the Opportunity Cost.

The Math of the “Small” Expense

Let’s take a classic example: a daily $7 habit (could be a premium coffee, an energy drink, or a fast-food snack).

-

Monthly Cost: $210

-

Annual Cost: $2,555

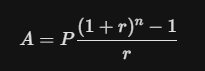

Now, let’s look at the hidden cost. If you invested that $210 a month into a broad market index fund with an average annual return of 8%, what would that look like over time?

After 30 years, that $7 daily habit has a hidden cost of approximately **$315,000**. You didn’t just buy a snack; you bought a luxury apartment in your retirement and threw the keys in the trash. When we view bad habits through the lens of opportunity cost, “small” expenses suddenly look much larger.

High-Interest Debt: The “Anti-Compounding” Machine

Compound interest is often called the eighth wonder of the world when it works for you. When it works against you—in the form of credit card debt—it is a financial death spiral.

The Minimum Payment Trap

Credit card companies are masters of behavioral psychology. They offer “minimum payments” specifically to keep you in the debt cycle for as long as possible.

Key Insight: If you have a $5,000 balance on a card with a 24% APR and you only pay the minimum, you will end up paying back nearly **$15,000** over the course of 20 years.

The hidden cost of bad credit habits isn’t just the interest; it’s the loss of mobility. Every dollar that goes toward interest is a dollar that cannot be used to start a business, travel, or buy a home. High-interest debt is a tax on your future self that provides zero utility today.

Lifestyle Inflation: The Moving Goalpost of Success

One of the most insidious bad habits is Lifestyle Inflation. This happens when your spending increases at the same rate (or faster) than your income. You get a $10,000 raise, and suddenly you “need” a $10,000 more expensive car.

Why You Feel Broke at Six Figures

Lifestyle inflation is why people earning $250,000 a year often report living “paycheck to paycheck.” They have traded their freedom for higher-quality “stuff.”

-

The Habit: Upgrading your life every time you get a win.

-

The Hidden Cost: You never build a “gap” between your income and expenses. Without that gap, you can never achieve true financial independence. You are essentially a high-paid prisoner of your own lifestyle.

The cost here is Time. If you maintain your lifestyle while your income grows, you could potentially retire a decade earlier. By inflating your lifestyle, you are effectively choosing to work ten extra years of your life to pay for a slightly nicer zip code or a leather interior.

The “Laziness Tax”: Failure to Negotiate and Review

Are you still paying for that streaming service you haven’t watched in six months? Is your car insurance rate the same as it was three years ago? If so, you are paying the Laziness Tax.

The Cost of Set-and-Forget

Companies rely on “Inertia Marketing.” They know that once they have your credit card on file, you are unlikely to leave.

-

Subscriptions: The average American spends over $200 a month on subscriptions, many of which are forgotten.

-

Insurance & Utilities: Failing to shop around for rates once a year can cost you between $500 and $2,000 annually.

Over a 40-year working life, the failure to spend two hours a year reviewing your bills has a hidden cost of over $100,000 (when adjusted for potential investment growth). Being “too busy” to check your statements is a very expensive personality trait.

Emotional Spending: The High Price of “Retail Therapy”

We live in an age of instant gratification. When we feel sad, bored, or stressed, the dopamine hit of a “Buy Now” button is a powerful drug.

The Psychology of the Purchase

Emotional spending is a bad habit because it uses a temporary solution (a new product) to solve a permanent problem (emotional health).

-

The Habit: Scrolling through shopping apps as a form of entertainment.

-

The Hidden Cost: Declining mental health and a cluttered home.

When you spend emotionally, you often buy items you don’t need, don’t use, and eventually have to pay to store or dispose of. The hidden cost is the Clutter Tax—the mental and physical space occupied by the debris of your past impulses.

Lack of an Emergency Fund: The “Everything is a Crisis” Tax

Living without an emergency fund is a habit of extreme risk. When you don’t have a cash buffer, a flat tire isn’t just an inconvenience; it’s a high-interest credit card debt event.

The Fragility of Your Finances

| Scenario | With Emergency Fund | Without Emergency Fund |

| Medical Bill | You pay the bill and move on. | You take a payday loan or use a credit card. |

| Car Repair | Stressful, but manageable. | You miss work because you can’t fix the car. |

| Job Loss | You have 6 months to find the “right” job. | You take the first “bad” job out of desperation. |

The hidden cost of not having an emergency fund is Desperation. When you are desperate, you make bad long-term decisions. You take jobs you hate and loans you can’t afford. A liquid cash reserve is the cheapest insurance policy you will ever buy.

The Health-Wealth Connection: Neglecting Your Body

It might seem out of place in a financial article, but neglecting your health is one of the most expensive financial habits you can have.

The Long-Term Medical Bill

A habit of poor nutrition, lack of exercise, or smoking has a massive back-end cost.

-

Short-term: Lower productivity and more sick days.

-

Long-term: Chronic conditions that require expensive medication, specialized care, and a shorter career.

The hidden cost here is Productivity and Longevity. If your health prevents you from working during your peak earning years (your 50s and 60s), you could be losing out on millions in lifetime earnings. Your body is the engine that generates your wealth—treat it like a high-performance machine, not a landfill.

Failure to Automate: The “Human Error” Cost

If you have to “remember” to save money every month, you eventually won’t. Relying on willpower is a bad habit because willpower is a finite resource.

The Power of Systems

The hidden cost of manual finances is the Inconsistency Tax.

-

The Habit: Waiting until the end of the month to see “what’s left” to save.

-

The Result: Nothing is usually left.

By failing to automate your savings and investments, you miss out on months of market growth. Automation removes the friction of “choosing” to be responsible. If the money is gone before you see it, you adapt your lifestyle naturally.

Financial Ostrich Syndrome: Ignoring the Truth

Many people have the habit of simply “not looking” at their bank accounts when they know they’ve overspent. This is Financial Ostrich Syndrome.

The Danger of Darkness

When you don’t know your numbers, you can’t improve them.

-

Hidden Cost: Late fees, overdraft charges, and missed opportunities to correct course.

-

The Mental Toll: Chronic, low-level anxiety. You might not be looking at the numbers, but your brain knows they are there.

The cost of this habit is Control. You cannot steer a ship if you refuse to look at the compass. Transparency with yourself is the first step toward freedom.

Turning the Tide on Your Habits

The hidden costs of bad financial habits are staggering, but there is good news: habits can be rewritten. You don’t need to change your entire life overnight. Start by identifying one “leak”—perhaps a forgotten subscription or a daily impulse buy—and redirect that money into an automated investment account. Once you see the power of that small change, the momentum will carry you forward.

Wealth isn’t something that “happens” to you; it is something you build, cent by cent, through the habits you choose to cultivate. Break the silent leaks today, and your future self will be sailing on much smoother waters.